On Saturday, Badan Warisan Malaysia (The Heritage of Malaysia Trust) had an interesting historical discussion worth noting by emerging and frontier market investors:

💻 BWM Talk Series: Revisiting the Guthrie Dawn Raid by Prof. Nicholas J. White

Malaya (as it was then known) at the time of its independence in 1957 was the world’s largest producer of tin and rubber. However, these industries were mostly foreign (i.e. British) owned. Unlike some developing countries, Malaysia did not seize or nationalise colonial assets by force. Instead, we did it in the most gentlemanly manner possible – we went to the London Stock Exchange to acquire these assets at full market prices!

The Guthrie Dawn Raid in 1981 remains a watershed in Malaysian corporate history. It paved the way for the localisation of and cessation of foreign control in plantation and trading companies which were previously established under colonial rule in Malaya such as Sime Darby, Boustead, Harrisons & Crossfields, Guthrie and many others.

About The Speaker

Prof Nicholas J. White of Liverpool John Moores University, UK will share fascinating insights from his extensive research and work on this topic.

The Malaysian business press has also done a few stories remembering the raid:

📰 Opinion — The Dawn Raid: How Malaysia outplayed the empire (The Edge Malaysia) 20 Aug 2025 🗃️

- On the morning of Sept 7, 1981, as London’s financial district stirred to life, something unusual happened. Shares of Guthrie Corporation — a British firm with vast plantations in Malaysia — were being snapped up at lightning speed. Confusion spread. Who was buying? Why?

- Within two hours, nearly 47% of Guthrie’s shares had been acquired. The Malaysian team, working discreetly through brokers and nominee accounts, had triggered a mandatory general offer. The raid was over before London could react.

- Malaysia had just reclaimed a colonial crown jewel — without breaking a single rule.

📰 Recalling the Guthrie Dawn Raid (NST Online) 1 Feb 2020 🗃️

- The Guthrie “Dawn Raid” by Permodalan Nasional Bhd (PNB), 38 years ago, on Sept 7, 1981, needs to be seen against this background. The raid was a fine-tuned and balanced initiative. The following is a brief account of now almost forgotten events, but a vital chapter in our nation’s history.

- CHRONICLING A VITAL CHAPTER

- I have been privileged to research and record a major milestone in our nation’s history. It was a long journey of almost four years that took me (together with co-researcher Nick White) to a small English town of Sherborne, Dorset, to interview the former Guthrie chairman, Mark Gent. And again, to Salisbury to talk to the late Sir Donald Hawley, the former British high commissioner to Malaysia when the raid took place.

📰 The Guthrie Dawn Raid remembered (The Star) 12 Sept 2021 🗃️

- The British investors were caught by surprise when they found themselves no longer in control of some 800sq km of agricultural land in Malaysia – hitherto a valuable and consistent source of revenue. Mark Gent, the Guthrie Corporation chairman, learnt of this acquisition in a news broadcast over the radio.

Guthrie was founded in Singapore in 1821 by Alexander Guthrie as the first British trading company in Southeast Asia who introduced rubber and oil palms to Malaya in 1896 and 1924. The company is often covered in books about the history of Malaysia or autobiographies/histories of “planters” in Malaya who worked for them.

It was also a FTSE 100 company, usually ranking around 65-68 at the time of the “raid,” meaning it was almost the equivalent of the Philippines taking over P&G or another storied American corporate or S&P/Dow name.

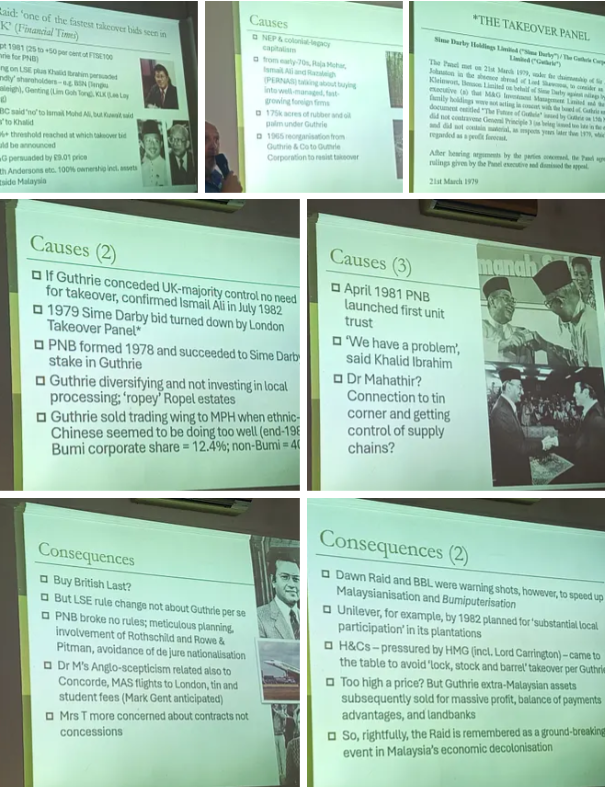

However, the British had been “sloppy” about Guthrie’s organization e.g. it was a mess of smaller companies and cross directorships that was forced by the LSE or British government to organize better under a holding company in the 1960s to make it harder for Malaysia to take control of it (ironically, this made it easier to wrestle control via legal means). However and despite PNB (and/or with other Malaysia/Singapore based interests owning smaller chunks) owning or controlling 25% of shares, the British refused to give Malaysians any Board seats with the Board/management still being based in London.

But Malaysia (being a multi-racial country with a parliamentary system/elections) could not simply nationalize foreign owned businesses (like what Indonesia or Burma did). This would have completely destabilized Malaysian society and harmed future investment in a country hungry for investments offering higher returns (as the first Malaysian investment trusts offered to locals proved so successful that there was a danger of running out of local investments that could produce high returns – hence the need to acquire or take control of well managed foreign businesses).

Malaysia had also attempted a share takeover in the past with the sticking point being the share price offered was felt to be too low for British investors (who, at the time, still included many so-called “widows and orphans” rather than large institutions who came to dominate investing…).

For the successful “Guthrie Dawn Raid,” PNB utilized a firm specialized in these sorts of lightening corporate takeovers (e.g. basically using jobbers to quickly buy floating shares after quiet negotiations with other large shareholders) along with the Rothschilds who were much better at secrecy. In fact, only a couple of key people ahead of time knew about the “raid” which was executed within 4 hours of the London market opening – one of the fastest hostile corporate takeovers in history.

PNB also offered £9.01 a share after the Trust representing the “widows and orphans” had indicated they would sell if an offer was made in the £9 range (shares were apparently trading closer to £6 before the takeover). Thus, the previous takeover failure was avoided.

White noted that the “Guthrie Dawn Raid” was not the first occurrence of this sort of hostile takeover strategy on the LSE or resource nationalism that avoided hostile nationalizations (where compensation disagreements would end up in international arbitration courts for years and harm foreign investment) as Afrikaner economic nationalism had led to South Africa and DeBeers to take over LSE listed mining interests using similar methods.

Interestingly enough, Malaysia/PNB had tried to convince Oversea-Chinese Banking Corp (OCBC) (SGX: O39 / FRA: OCBA / FRA: OCBB / OTCMKTS: OVCHY) to pledge shares prior to the raid and for whatever reason, they refused (the Kuwait investment fund accepted instead). Up until then, Singapore based OCBC was more or less treated as a local bank in Malaysia. However, newly installed Prime Minister Mahathir remembered their refusal and OCBC’s started having a much more difficult time operating in Malaysia…

Another interesting footnote: Had Guthrie’s London-based Board simply transferred control (50.01%) to Malaysia based investors with the Board/HQ being Malaysia-based, Malaysia would have been satisfied and not taken the risk or cost of doing the “raid” for a complete takeover. After all, commodity prices were falling and it was later felt that Malaysia had paid too much for Guthrie.

However, Guthrie’s London-based Board was trying to diversify the Company away from Malaysia and commodities by buying/making unrelated businesses/investments in the USA and UK. Naturally, Malaysia did not like profits being made in Malaysia only to be remitted to London rather than being invested back in the country. These unrelated businesses (which apparently included an investment in a USA airline of all things…) were actually sold off for a profit that more than compensated for the share price Malaysia paid for the company.

A quick look at the 🇲🇾 Malaysia (98) section of our Southeast Asia Stock Index also reveals what could have happened had Guthrie’s London-based Board been a little less “sloppy” (and perhaps less “arrogant”):

- 🇲🇾 British American Tobacco (Malaysia) Bhd (KLSE: BAT / OTCMKTS: BATMF) – Leading legal tobacco company in Malaysia. 🇼

- 🌏 Carlsberg Brewery Malaysia Bhd (KLSE: CARLSBG) – Began brewing Carlsberg beer locally in 1972. Operations mainly in Malaysia & Singapore, + stakes in a brewery in Sri Lanka. Regional exports. 🇼 🏷️

- 🇲🇾 DKSH Holdings (Malaysia) Bhd (KLSE: DKSH) – Market expansion services provider. Subs. of DKSH Holding AG (SWX: DKSH / FRA: DS5 / OTCMKTS: DKSHF).

- 🇲🇾 Heineken Malaysia Bhd (KLSE: HEIM) – Produces, packages, markets, & distributes alcoholic beverages primarily in Malaysia. 51% held indirectly by Heineken NV (AMS: HEIA / FRA: HNK1 / OTCMKTS: HEINY) via its wholly owned subs. GAPL Pte Ltd. 🇼 🏷️

- 🇲🇾 Nestle Malaysia (KLSE: 4707 / OTCMKTS: NSLYF) – Manufactures & sells food & beverage products. Subs. of Nestlé SA (SWX: NESN / OTCMKTS: NSRGF). 🇼 🏷️

These foreign businesses saw the writing on the wall and undertook strategies that turned out to be a win-win for everyone involved and similar listing situations for local MNC units can be found in Indonesia, India, Nigeria, etc.

I should note that the storied Guthrie name does live on (albeit on a much smaller scale) as Sime Darby Bhd (KLSE: SIME / OTCMKTS: SMEBF) [Trading conglomerate. Automotive & industrial equipment brands. 🇼] revived the name in 2024 when they rebranded Sime Darby Plantation:

- 🌐 SD Guthrie Bhd (KLSE: SDG / OTCMKTS: SDPNF) – Upstream & downstream palm oil + land development & renewable energy. 🇼 🏷️

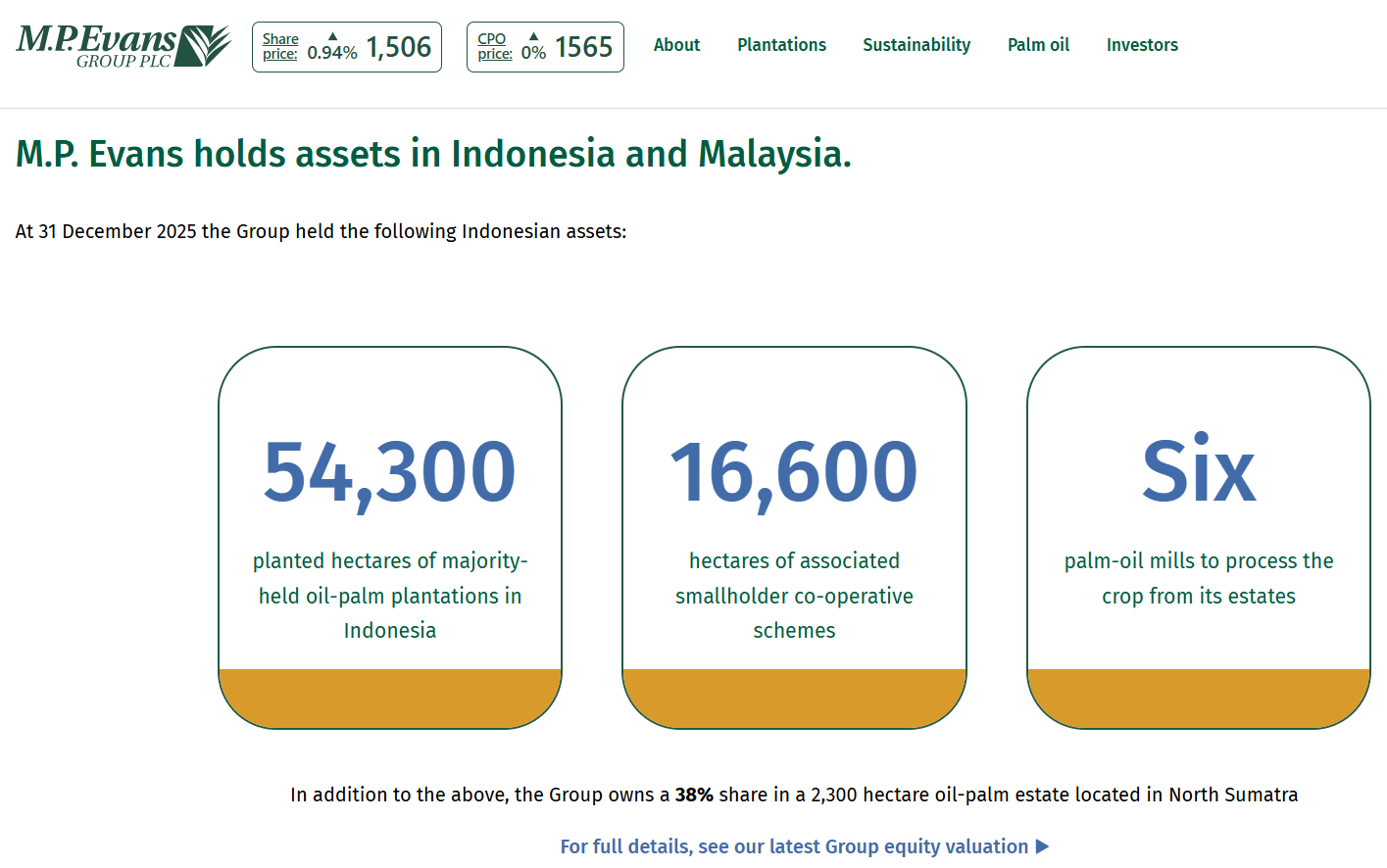

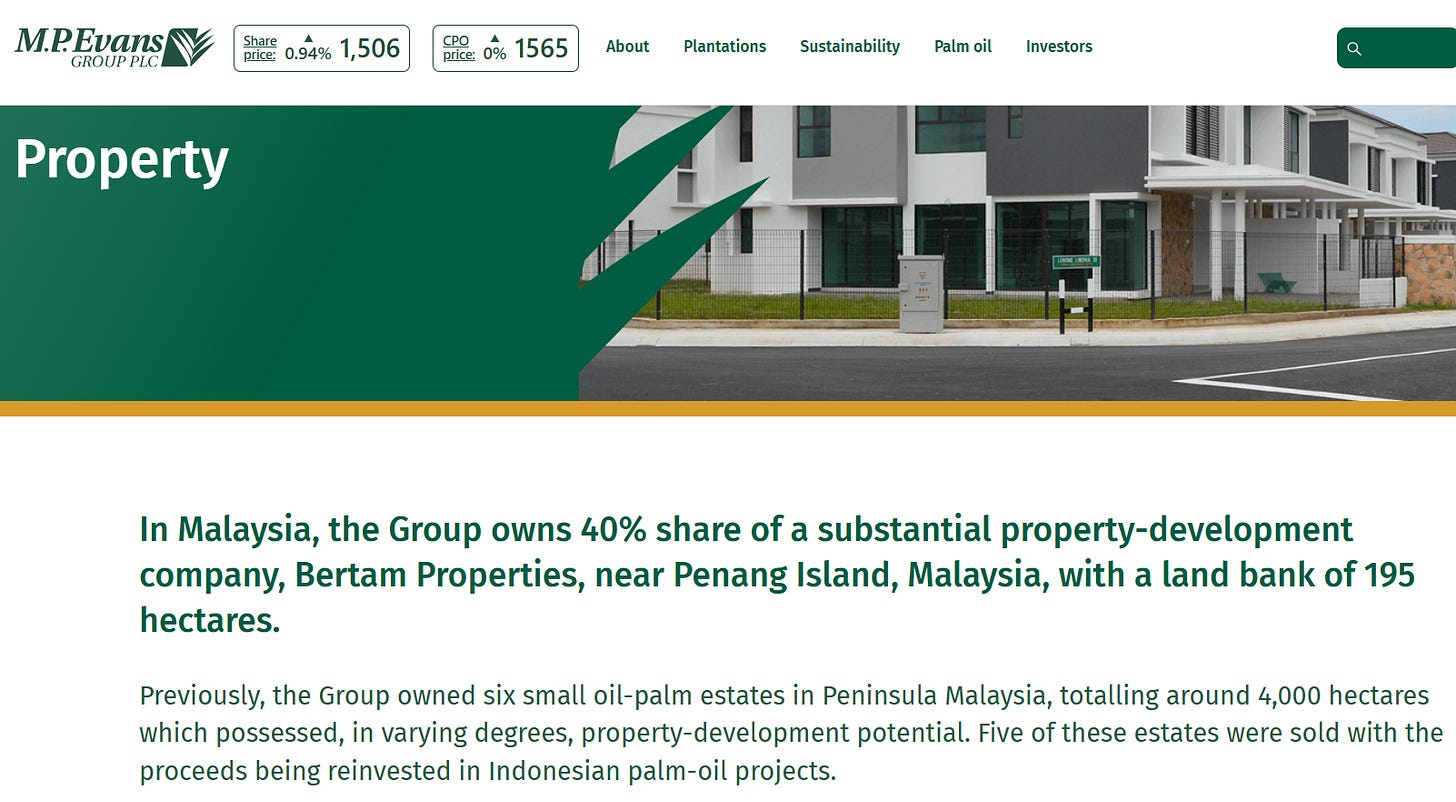

Otherwise, I’m mainly aware of one remaining “historical” (dating back to the 1870s) London based commodities player in Malaysia, or rather focused almost entirely on “sustainable” Indonesian palm oil now, with one particular British family apparently involved in the company since the 1940s (Note: It came up as a holding of a fund covered in June 21st post and the stock is worth a closer look by funds who have concerns about corporate governance in Indonesia/SE Asia or “sustainability” issues with ag and especially palm oil related investments):

- 🇮🇩 🇲🇾 MP Evans Group PLC (LON: MPE / FRA: NYP / OTCMKTS: MPEVF) – Palm plantations in Indonesia + investment in a property company in Malaysia.

Their website also indicates a focus on providing a decent dividend:

- Price/Book (Current): 1.72

- Forward P/E: 12.55 / Forward Annual Dividend Yield: 4.03% (Yahoo! Finance)

As of the start of July, more fund updates (our continuously updated post containing all funds is here) along with new emerging market research starting with some non-EM pieces pushing Europe:

- 🎥🇪🇺 Citywire Big Broadcast: Quality, value and the long game (Citywire via Fidelity) 51:33 Minutes – Marcel Stötzel, Co-Portfolio Manager of Fidelity European Trust PLC, joined Citywire’s Ian Horne to explain why his team is backing European domestic companies for the first time in 17 years. He also shares the key themes shaping his thinking, where he sees value today, and the challenges still facing markets.

- 🔬🇪🇺 A value-based case for today’s European banks (Robeco) – European bank stocks have enjoyed a multi-year run of strong performance, outpacing the STOXX 50 Index since early 2024 amid increased profitability. Today’s European banks are doing what US banks did from 2013-2019: rebuilding capital, restructuring cost bases, and returning to double-digit returns on equity.

🗄️ Fund documents / updates; ⚠️ Disclosures or restricted access e.g. based on your location, investor status, etc.; 🇼 Wikipedia page; 🔬 Research analysis (including articles/blog posts from fund managers, etc.); 🎥 Video; 🎙️ Podcast; 🎬 Webinar; 📝 Transcript; 📰 Newspaper/magazine article; 📯 Press release; 💻 Substack/blog/website article; ✅ Our own posts; 🗃️ Linked archived article; ⏰ Upcoming webinar or event.

📈 Contributors; 📉 Detractors; 🏧 Transactions; 🚩Discusses/mentions stocks by name.

Disclaimer: We usually use Deepseek to summarize or extract stock names and assign performance emojis. Like all AI, Deepseek is not perfect and regularly adjusts their model which can lead to mistakes/misunderstandings/misinterpretations of the data its given. Your use of any content is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the content.

🌏 New Asia Fund Documents & Research

- 🎬🌏 Rated by Kepler – Aberdeen Asia Focus (Kepler Trust Intelligence) 46:05 Minutes – Gabriel Sacks, Lead Manager of Abrdn Asia Focus PLC (LON: AAS), joins the Rated by Kepler 2026 webinar series.

To read more, please visit this article on Substack

Similar Posts:

- Investing in Malaysia ADRs / Malaysia Stocks List

- Malaysian Elections: Will The Malaysia ETF Rally or Sink?

- Investing in Malaysia ETF / Malaysia ETF List

- EM Fund Stock Picks & Country Commentaries (May 5, 2024)

- EM Fund Stock Picks & Country Commentaries (August 15, 2023)

- Bursa Malaysia (KLSE) (Profit Hunting blog)

- EM Fund Stock Picks & Country Commentaries (April 18, 2023)

- EM Fund Stock Picks & Country Commentaries (February 14, 2023)

- EM Fund Stock Picks & Country Commentaries (December 8, 2024)

- EM Fund Stock Picks & Country Commentaries (March 21, 2023)

- Public Bank (KLSE: PBBANK / OTCMKTS: PBLOF): Consistently Strong Financial Performance & Prudent Management

- EM Fund Stock Picks & Country Commentaries (June 20, 2023)

- EM Fund Stock Picks & Country Commentaries (June 8, 2025)

- Falling Oil Prices Puts a Spotlight on Malaysia’s Debt (Reuters)

- EM Fund Stock Picks & Country Commentaries (June 30, 2024)