Emerging Market Links + The Week Ahead (October 13, 2025)

by

Vietnam has been upgraded to emerging market status by FTSE Russell🗃️in a move that could potentially bring in billions of dollars in active investment and around $500 million in passive inflows (the status will take effect next September pending an interim review in March). The Financial Times noted:

MSCI classifies Vietnam as a frontier market but the country aims to earn an MSCI upgrade to emerging market by 2030. It is pushing to be classified as an “advanced emerging market” by FTSE by the same date and plans further reforms to meet the stricter criteria.

Investing in Vietnam from overseas has long been challenging. It can take months for investors to acquire the identification needed for the market and foreigners pay a premium for shares of some companies due to limits on non-Vietnamese ownership, said Owens Huang, a portfolio manager at Dalton Investments.

Personally, I would be very leery of investing in individual stocks in Vietnam (if you have lived in or done business there, you will understand why…); but investing in active funds with a long presence there or a well diversified ETF (VanEck Vietnam ETF (BATS: VNM))could make sense for retail investors.

Growing AI bubble worries, flying car test flights, Vietnam upgraded to EM status by FTSE Russel, investing where pessimism reigns, Mauritius investment landscape, Middle East trip report, etc.

📰🔬 Emerging Market Stock Picks / Stock Research

$ = Behind a paywall / 🗃️ = Link to an archived article / ⛔ = Article archiving may not be working properly

Summary: This post is an attempt to figure out whether the appointment of Sanae Takaichi as the next Prime Minister will have any implications for Japanese equities. She’s a conservative who’s hawkish when it comes to geopolitics but dovish when it comes to monetary policy. It looks like she will continue Shinzo Abe’s push for corporate reform. This combination should be bearish for the Japanese Yen and bullish for Japanese equities, especially within the nuclear and defense industries.

Sanae Taikichi will become the next Prime Minister of Japan. This is likely to have a Negative impact on the Korean automakers including Hyundai Motor (KRX: 005380 / FRA: HYU / OTCMKTS: HYMTF) and Kia Corp (KRX: 000270 / OTCMKTS: KIMTF).

Sanae Takaichi is a firm advocate of the late Prime Minister Shinzo Abe’s “Abenomics” strategy to boost the economy with aggressive spending and easing monetary policy.

The weakening JPY combined with existing tariff rate advantage versus the South Korea could further positively impact the Japanese auto makers versus the Korean auto makers.

Chinese stocks listed on the Chinese mainland and in Hong Kong attracted a net inflow of $4.6 billion from long-only U.S. and EU funds last month, marking the highest monthly level in nearly a year, according to a Morgan Stanley report.

The largest inflow since November 2024 was driven by passive funds, whose inflows totaled $5.2 billion, according to the report published last week. Meanwhile, active funds saw an outflow of $600 million.

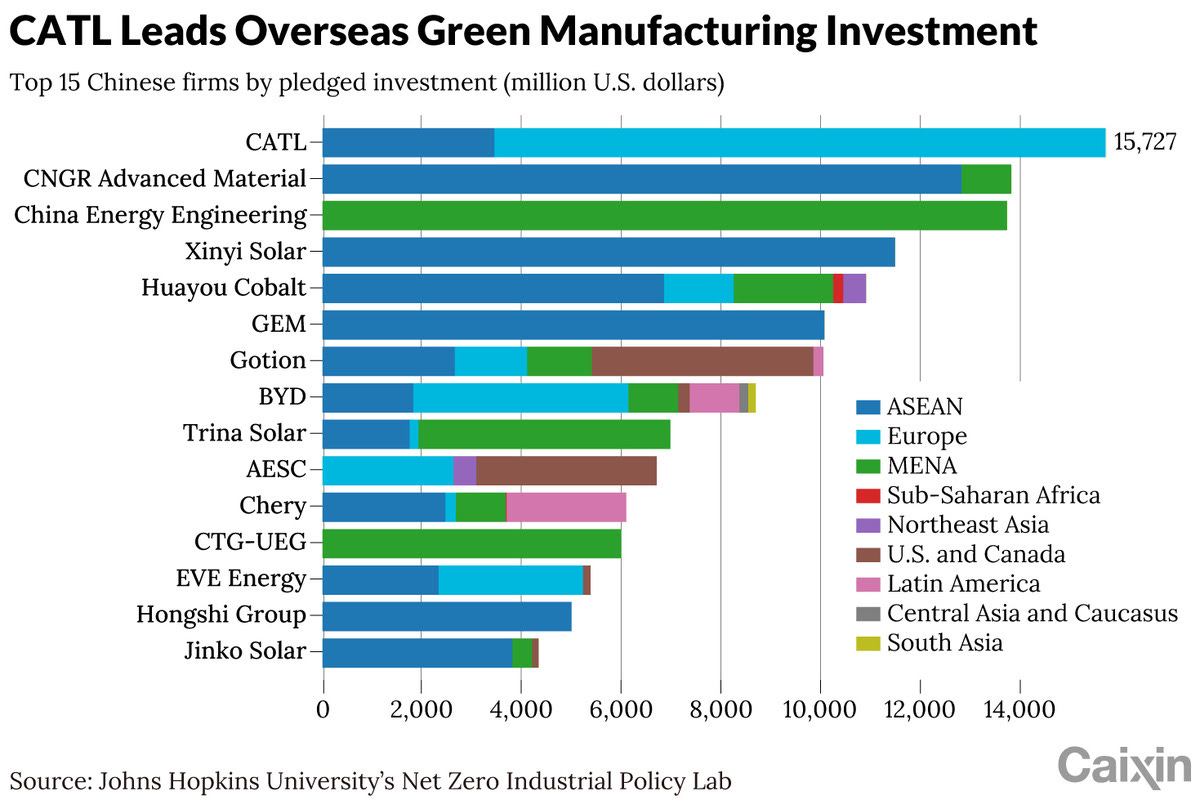

The world’s largest electric-vehicle (EV) battery maker has pledged $15.7 billion in total, beating battery-ingredient producer CNGR Advanced Material Co. Ltd. and state-owned energy conglomerate China Energy Engineering Corp. (CEEC), according to an analysis by the Net Zero Industrial Policy Lab at Johns Hopkins University.

Business focus moves to unit order earnings as market shares stabilize

The ever-lasting battle among the three food delivery platforms in China – Meituan (HKG: 3690 / 83690 / SGX: HMTD / FRA: 9MD / OTCMKTS: MPNGF / MPNGY), Alibaba (NYSE: BABA) and Jingdong – is likely to enter into a new stage with their operating losses expected to peak in the third quarter of 2025 and gradually narrow thereafter, according to a recent report from US investment bank Jefferies.

The high-profile entry of Jingdong in February and Alibaba in May is reshaping China’s food delivery sector, which used to be dominated by Meituan and quickly escalated into an industrial turf war that burnt through an estimated US$4 billion in operating expenses in the second quarter alone.

Alibaba (NYSE: BABA)’s stock has staged an impressive rebound, climbing sharply after its latest earnings call. The numbers themselves were hardly eye-catching, but investors focused on something different.

Management stressed a new story built around cloud computing, artificial intelligence, and overseas growth.

That shift in focus gave the market a reason to take a fresh look at the company, even as challenges in its core e-commerce business remain.

Earnings Breakdown

Growth Engines Driving the Rally

Beyond Earnings and AI: The Food-Delivery Price War

Get Smart: Alibaba’s stock bounced not on the numbers, but on the narrative

Meituan (HKG: 3690 / 83690 / SGX: HMTD / FRA: 9MD / OTCMKTS: MPNGF / MPNGY), China’s largest food delivery platform, has launched into the U.S. market.

But Meituan’s U.S. entry is not via its international food delivery subsidiary Keeta.

Instead, it launched a POS/restaurant SaaS system in the U.S. called Peppr, directly challenging industry leaders like Toast and Square in a crowded market.

Peppr’s slogan, “The only POS built for how restaurants actually operate,” showcases how it wants to be perceived. The brand focuses on family-owned mom-and-pop restaurants across the United States.

PDD Holdings (NASDAQ: PDD) orPinduoduo’s second-quarter 2025 financial results reflect a strategic focus on long-term value creation rather than short-term financial gains.

The company’s revenue for the quarter increased by 7% year-over-year to RMB 104 billion, driven primarily by online marketing services and transaction services.

However, operating profit experienced a significant decline of 21% year-over-year, reflecting the company’s substantial investments in enhancing its platform ecosystem through its RMB 100 billion support program aimed at bolstering merchant capabilities and fostering sustainable growth.

The Chinese maker of photovoltaic inverters is tapping investors to fund a deeper push into the energy storage and supply business as AI demand takes off

The company supplies a quarter of the world’s photovoltaic inverters and nearly 12% of energy storage systems

The energy storage business accounted for 41% of the firm’s revenue in the first half, surpassing its inverter income for the first time

Chery Automobile Co Ltd (HKG: 9973) made a strong debut on the Hong Kong Stock Exchange Thursday, raising HK$9.2 billion ($1.2 billion) in the city’s largest carmaker IPO of the year and seeing its shares soar as much as 11.2%.

Shares closed at HK$31.90, up 3.7% from the IPO price of HK$30.80, giving the company a market capitalization of HK$184 billion — placing it nearly on par with rival Geely Automobile Holdings (HKG: 0175 / FRA: GRU / OTCMKTS: GELYY / GELYF).

The listing marks a major milestone for the state-owned automaker, founded in 1997, after several failed attempts to go public.

The veteran car group will privatize its namesake brand and simultaneously spin off its Voyah brand for a new listing to stay competitive in fast-evolving NEV market

Dongfeng Motor Group Co Ltd (HKG: 0489 / FRA: D4D / D4D0 / OTCMKTS: DNFGF / DNFGY) plans to list its Voyah NEV unit, which turned profitable in the first seven months of this year from a year-ago loss

The brand sold 80,000 vehicles in the first eight months of this year, matching its total for all of last year

Zhuzhou CRRC Times Electric (SHA: 688187 / HKG: 3898 / FRA: ZTX / ZTX0 / OTCMKTS: ZHUZY) as the name suggests is a part of the CRRC (China Railway) corporate umbrella and is based out of Zhuzhou, Henan Province, China. Zhuzhou, a satellite city of Changsha, is a major Chinese hub for heavy machinery production and one of the sites of production for the Chinese railway sector. The company’s origins trace back to the 1950s and 60s with the Zhuzhou Electric Locomotive Research Institute that was instrumental in China’s early development of railway technology. TEC was officially established in 2005, consolidating several specialist units from the former CSR Group, and renamed following the merger that created CRRC in 2015. Over the last six decades, it has led China’s transition from DC to AC traction systems and been instrumental in developing the electrical systems powering China’s high-speed rail network, the world’s largest today. The scope of TEC’s business extends far beyond rail systems today. It manufactures and develops a wide range of products like traction converters, motors, transformers, control systems, braking systems, and onboard electronics. The company also develops engineering vehicles utilized in rail infrastructure maintenance and is increasingly focusing on areas like photovoltaic inverters, industrial converters, and electric drive systems for NEVs.

The personal finance platform’s gross margin rose by 16 percentage points in the second quarter, as it focused on its higher-margin insurance and wealth segments

MoneyHero Ltd (NASDAQ: MNY)’s adjusted EBITDA showed strong sequential improvement in the second quarter as it concentrated on higher-margin products and achieving greater efficiencies

Under a CEO appointed last year, the company’s shares have rallied on growing investor confidence in its path to profitability.

The Shanghai-traded futures company is seeking a second listing at a time when growing economic uncertainty may lead to greater demand for its services

Nanhua Futures(SHA: 603093) has been approved by Chinese regulators for a Hong Kong IPO to supplement its current Shanghai listing

The new share offering would come as the futures company steps up its overseas expansion to meet demand from Chinese businesses going global

Midea Group (SHE: 000333 / HKG: 0300 / FRA: 1520 / OTCMKTS: MGCOF)will achieve double-digit growth in 2025. As domestic home appliance market enters a stage of competition for existing customers, B-end market and overseas markets have become new growth keys.

The development path of three giants becomes clear – Midea pursues full industry chain synergy with diversified layout/digital capabilities. Haier Smart Home (SHA: 600690 / HKG: 6690 / OTCMKTS: HSHCY / OTCMKTS: HRSHF) builds a global brand matrix through high-end/localized operations. Gree Electric Appliances Inc of Zhuhai (SHE: 000651) is lagging behind.

For mature industry leading enterprises, 10-18x P/E is reasonable, or market value of RMB430-855bn based on Midea’s 2025 net profit forecast. Considering higher growth, valuation would be higher than Haier.

The leading milk tea chain will pay $40 million for 51% of Fulujia, one of the country’s leading operators of stores selling beer-based drinks

MIXUE Group (HKG: 2097 / OTCMKTS: MXUBY) will pay 285.6 million yuan for a majority stake of a major beer drink store operator, as it expands beyond the crowded bubble tea sector

The acquired company, Fulujia, is controlled by the wife of Mixue’s CEO, but the two sides appear to have negotiated a fair price for the purchase

China’s third largest pop toy seller, a spinoff of Japanese-style retailer MINISO Group Holding (NYSE: MNSO), has filed for a Hong Kong IPO just five years after its founding

Miniso spinoff Top Toy has filed to list in Hong Kong, aiming to leverage its parent’s network of 7,000 global stores as it seeks to copy Pop Mart’s success

A $1.3 billion valuation and growing stable of self-developed intellectual property could boost the toymaker’s chances of success in an increasingly crowded field

The online medical services provider raised about $20 million after pricing its shares at the bottom of their range – below a Nasdaq-proposed new minimum threshold of $25 million

PomDoctor Ltd (NASDAQ: POM) priced its IPO shares at the bottom of their range, seeking a high P/S ratio of nearly 10 that values the company at $472 million

The company was racing to complete its listing before the rollout of new Nasdaq rules that will require all new foreign listings to raise at least $25 million

JST Group (1703609D CH) is China’s largest e-commerce SaaS ERP provider. It is seeking to raise US$250 million to US$300 million.

JST (Jushuitan) is China’s largest e-commerce SaaS ERP provider in terms of relevant revenue in 2024, with a market share of 24.4%, according to CIC.

The investment case is bullish due to robust book-to-bill ratios, strong growth, high contract liabilities, underlying profitability and cash generation.

Guangdong Chj Industry Co A (SHE: 002345) (CHJ) submitted an application to list H-shares on the Main Board of the Hong Kong Stock Exchange.

Despite higher valuation multiples, the company has been able to successfully generate higher sales and profits in the past several years.

The high and rising global gold prices have created a strong loyal customers and investor base that could positively impact this IPO on the HK Stock Exchange.

CHJ plans to use some of the funds from the new listing for 20 overseas stores, three new domestic flagship stores, and a new production base. CHJ was established in the city of Shantou in South China’s Guangdong province in 1996, and is known as the “King of K-gold” due to its longstanding focus on design and use of gold alloys.

Chinese energy drink giant Eastroc Beverage Group Co Ltd (SHA: 605499) has filed once again for a Hong Kong listing, just days after its previous application expired.

The Shanghai-listed company, known for its flagship “Eastroc Energy Drink,” submitted a new application to the Hong Kong Stock Exchange (HKEX) on Oct. 9, with Huatai International, Morgan Stanley, and UBS serving as joint sponsors. Eastroc aims to become a dual-listed “A+H” company.

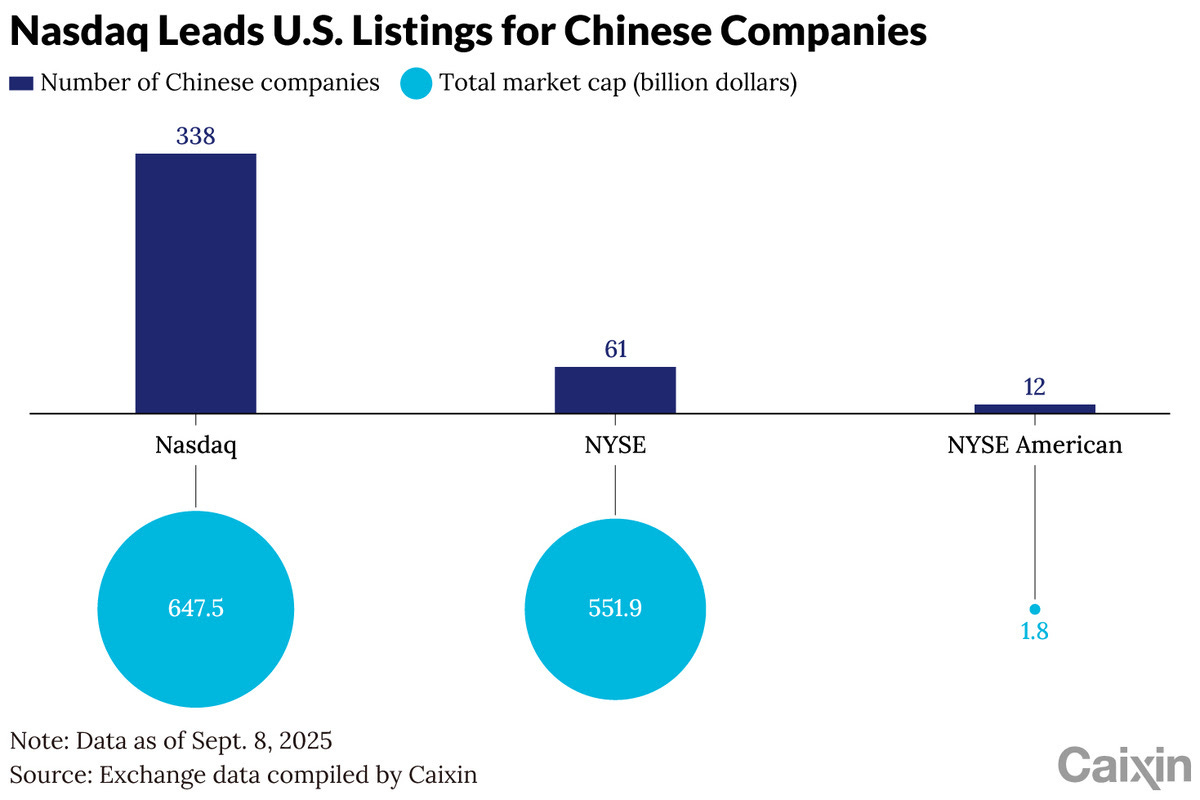

Chinese companies pursuing overseas listings are at a crossroads.

For years, the U.S. — and especially the Nasdaq — has been a preferred market for Chinese IPOs, offering companies high valuations and access to a global investor base. But that path may be narrowing.

The tech-heavy bourse, which hosts more than 80% of U.S.-listed Chinese firms, has proposed raising the minimum public float and fundraising requirements, while enforcing faster suspension and delisting procedures for companies that fail to meet ongoing standards, casting uncertainty over the pipeline of future deals.

Shares of Hang Seng Bank Ltd (HKG: 0011 / FRA: HSB / OTCMKTS: HSNGY) jumped by nearly 26% Thursday after the announcement that its controlling shareholder HSBC Asia Pacific plans to take the Hong Kong-based lender private in a HK$106 billion ($13.6 billion) deal.

HSBC Asia Pacific, which already holds around 63% of Hang Seng Bank, has proposed buying the remaining shares for HK$155 apiece, about 30% above its closing price Wednesday, according to HSBC Asia Pacific’s proposal released early Thursday.

🌐 Prenetics Global Ltd (NASDAQ: PRE) – Multi-cancer early detection technologies + IM8 (health & wellness brand) & Europa (sports distribution in the USA). 🇼

Blue chip Chinese Rolex dealer at 8x P/E and 50% net cash/market cap

Our friends at TickerTrends recently wrote about an ongoing turnaround in the luxury wristwatch market. The data is clear: in the past four months, an index of Google search queries for the keyword “Rolex” have shot up. Second-hand prices for Rolex watches have risen for the first time since 2022.

So what’s going on? That’s what I’ll try to find out in this new deep-dive on Hong Kong’s Oriental Watch (HKG: 0398) — US$214 million) – the most “blue chip” of the publicly listed watch retailers in China.

But first, let’s talk about the industry. Oriental Watch and its publicly listed peers Emperor Watch & Jewellery Ltd (HKG: 0887 / FRA: EPU / OTCMKTS: EPRJF) and Hengdeli Holdings Ltd (HKG: 3389 / FRA: XYUA / OTCMKTS: HENGF / HENGY) are authorized dealers for Rolex in Hong Kong and Mainland China. Rolex remains the most sought-after luxury wristwatch brand, and has performed well despite new competition from the Apple and Garmin.

Macau’s visitor tally for this year’s eight-day October Golden Week was just above 1.14 million, according to data published by Macau’s Public Security Police.

The figure was up 15.3 percent from the festive period a year earlier. In 2024, the holiday ran for seven days, i.e., October 1 to 7, during which time Macau welcomed 993,117 visitors, according to official data.

October Golden Week is a major festive break for mainland China consumers and a peak trading period for Macau’s casinos. Mainland China is the main feeder market for Macau’s tourism sector.

China’s State Council had designated this year’s holiday period on the mainland as running from October 1 to 8, encompassing China’s National Day on October 1, and the lunar calendar-based Mid-Autumn Festival, which this year fell on October 6.

The president and chief operating officer of the United States-based casino firm Las Vegas Sands (NYSE: LVS), Patrick Dumont, says the company is looking to bring more high-profile sports events to its Macau properties.

Mr Dumont’s comments came as the firm’s Macau subsidiary, Sands China (HKG: 1928 / FRA: 599A / OTCMKTS: SCHYY / OTCMKTS: SCHYF), hosted two 2025 pre-season games between National Basketball Association (NBA) teams – the Phoenix Suns and the Brooklyn Nets – on Friday and Sunday, respectively.

“Macau really is a city of entertainment and sport,” Mr Dumont said during a fireside chat (pictured) on Sunday.

“Because of the format here, it’s easy to organise other sporting events. So, the goal is to bring more sports here over time and highlight that capability.”

Hahn & Co, holding 21.63% of Hanon [Hanon Systems (KRX: 018880)], won’t join the rights issue, raising the odds of a CJ CGV–style stock rights dump hitting the market.

Hanon’s rights float mirrors CJ CGV (~17% post-ESOP), with Hahn & Co likely to sell, limited local demand, and potential follow-on selling pressure.

Hanon’s 50% rights at 15% discount offer smaller float than CJ CGV, but larger deal size and weak EV sentiment create a potential CJ CGV–style arb, with SSF tradability.

One of the key emerging catalysts for Flitto is the rapid adoption of the company’s AI-based simultaneous interpretation solution called Live Translation by companies such as Apple.

Global big tech companies such as Apple, Meta, and Amazon Web Services (AWS) have used the service for their own events, which has accelerated its growth.

Flitto had its best ever quarterly results in 2Q25. It had sales of 9.4 billion won (up 156% YoY). Operating margin surged from -38.5% in 2Q24 to 25.9% in 2Q25.

Our NAV analysis of Samsung C&T Corp (KRX: 028260 / 02826K) suggests implied market cap of 43 trillion won or target price of 253,146 won per share which is 28% higher than current price.

The biggest components of Samsung C&T’s value is its stakes in Samsung Electronics (KRX: 005930 / 005935 / LON: BC94 / FRA: SSUN / OTCMKTS: SSNLF) and Samsung Biologics (KRX: 207940) which are worth 54.1 trillion won (161% higher than Samsung C&T’s current market cap).

In the past three months, the share price discrepancy between Samsung Electronics and Samsung C&T is more noticeable (Samsung Electronics – up 47.3% versus Samsung C&T – up 15.9%).

Our base case valuation of Aimedbio is implied market cap of 882 billion won or target price of 13,256 won per share over a one year view in 2026.

This represents 21% upside over a one year period. Our cumulative sales and operating profit estimates from 2025 to 2029 are 11.4% and 48.3% lower than the company’s estimates, respectively.

Aimedbio is not an easy company to value. Core investment thesis of the company is that it has an excellent technologies for antibody-based therapeutics, primarily antibody-drug conjugates (ADCs).

Recycling Rupiah into a deep value packing leader with competitive margins and rising dividends

Indonesia’s plastic packaging industry may not be shiniest, most headline-grabbing EM play, but this Company is among the leanest in the business, with a grip on traditional markets that multinationals will struggle to match. Panca Budi Idaman Tbk PT (IDX: PBID); “Panca Budi”) generates high returns on minimal leverage, compounding quietly while others chase growth at any cost. With rising dividend payouts, near-zero net debt, and a moat built on distribution and consistency, this name is an overlooked yield play in Southeast Asia’s largest consumer market.

The offer to minority shareholders is equivalent to RM2.35 per share, according to the takeover notice posted to Bursa Malaysia on Monday. The price tag is a premium of nearly 10% to Genting Malaysia’s last price of RM2.14 last Friday before trading of the stock was suspended for the announcement.

The offer is conditional upon Genting receiving enough acceptance to raise its shareholding above 50% of the voting shares in Genting Malaysia.

Currently, Genting holds a 49.36% stake in Genting Malaysia.

The privatisation, if successful, would be the largest acquisition in more than four years and comes at a time when Genting Malaysia is bidding for a casino licence in New York as part of a US$5.5 billion (RM23.19 billion) resort development in Queens.

Genting Berhad(KLSE: GENTING / OTCMKTS: GEBHY), a Malaysia-based conglomerate with global casino interests, has acquired an aggregate of 1,727,200 ordinary shares in a listed subsidiary, casino operator Genting Malaysia(KLSE: GENM OTCMKTS: GMALY / GMALF). That is according to the latter’s Thursday announcements filed with Bursa Malaysia.

Genting Berhad had acquired 900,000 ordinary shares in Genting Malaysia on Tuesday (October 7), and another 827,200 shares on the following day.

Lim Kok Thay – the head of gaming conglomerate Genting group – has a deemed interest in the Genting Malaysia shares acquired by the parent. That is via Mr Lim being a beneficiary of a discretionary trust, of which an entity called Parkview Management Sdn Bhd is the trustee.

Philippines-listed gaming technology providerPhilWeb Corp (PSE: WEB) announced on Thursday that its majority shareholder, Gregorio Araneta Inc, has signed an agreement to sell its entire stake in PhilWeb for a total consideration of PHP1.80 billion (US$31.0 million), equivalent to 829.57 million common shares at PHP2.17 apiece.

The buyers were identified as Philippines-based Nexora Holdings Inc and Velora Holdings Inc. Both firms were described in PhilWeb’s disclosure as domestic holding companies that are not engaged in securities brokering.

Philippines-listed and -licensed online gaming operator DigiPlus Interactive (PSE: PLUS) announced on Friday what it described as a “strategic pause” of its first Brazilian brand, GamePlus. The suspension of operations took effect immediately.

The announcement came weeks after September 22, when DigiPlus launched GamePlus – its first international brand – in the South American nation.

“Over the past three weeks, DigiPlus has used the soft-launch period as a live learning laboratory, capturing valuable insights into Brazilian player behaviour, cultural preferences, and entertainment dynamics,” the firm said in a press release.

If semi-annual reporting makes you nervous about a stock holding, that’s not a reporting problem — it’s a conviction problem.

The Singapore Experiment

Back in February 2020, Singapore made semi-annual reporting the new minimum standard for its stock market.

In hindsight, the timing couldn’t have been worse — the world was about to shut down for a pandemic — but the results are telling.

When given the choice, most companies jumped at the chance to report less often.

Singapore Exchange Limited(SGX: S68 / FRA: SOU / SOUU / OTCMKTS: SPXCF / SPXCY), the bourse operator itself, switched to semi-annual reporting, setting the tone for others to follow. The message was clear: if the stock exchange itself doesn’t offer quarterly updates, why should anyone else?

DBS Group (SGX: D05 / FRA: DEVL / DEV / OTCMKTS: DBSDY / DBSDF) continued reporting quarterly results, fielding questions from media and analysts every three months.

Income investors should focus on the stability and sustainability of the dividends they receive from companies; in this article, we take a look at three Singapore names that have maintained reliable pay-outs for more than a decade.

DBS Group Holdings: Singapore’s Largest Local Bank

DBS Group (SGX: D05 / FRA: DEVL / DEV / OTCMKTS: DBSDY / DBSDF) or DBS, is Singapore’s largest local bank with a strong track record of growing dividend payments backed by increasing profits and robust capital ratios.

UMS Integration manufactures high-precision components and equipment modules for original equipment manufacturers of semiconductors, while also serving aerospace and oil & gas industries, and water disinfection systems.

Union Gas Holdings Ltd supplies fuel products across Singapore through three segments: gas fuel (LPG, natural gas, and CNG), liquid fuel (diesel and petrol), and emerging businesses in EV charging and industrial gases.

Discover three Singapore dividend stocks offering 5% yields, backed by solid cash flow and reliable business fundamentals.

QAF Ltd (SGX: Q01)won’t win awards for earnings growth right now, but it’s got something dividend investors care about: a fortress balance sheet and the willingness to keep paying out.

The company manufactures and distributes bakery products across Southeast Asia and Australia, with operations spanning bread, confectionery, logistics, and a 50% stake in Malaysia’s Gardenia Bakeries joint venture.

Valuetronics Holdings (SGX: BN2 / FRA: GJ7)isn’t a household name, but it’s the kind of company that keeps global electronics supply chains humming.

HRNetGroup (SGX: CHZ)is Asia’s answer to a sprawling recruitment empire, operating across 18 Asian cities with over 900 consultants, and 20 brands built over 33 years.

Here’s something that may catch your eye: the conglomerate is one of Asia’s largest real estate investment managers with S$117 billion in funds under management (FUM) as of 13 August 2025.

Wilmar International: Total Return -3.7% for September 2025

Unlike the operational issues at Singtel, Wilmar International (SGX: F34 / FRA: RTHA / RTH / OTCMKTS: WLMIF / WLMIY) is facing regulatory challenges in Indonesia.

On 25 September 2025, the commodities conglomerate was fined close to US$710 million after the Indonesian Supreme Court overturned an earlier decision to acquit three of its subsidiaries.

Singapore’s green transition is unlocking opportunities for companies poised to benefit from the nation’s path toward net-zero by 2050.

Sembcorp Industries (SGX: U96 / FRA: SBOA / OTCMKTS: SCRPF)has transformed from a traditional fossil fuel-dependent-utility into a renewable energy powerhouse.

Compared to Sembcorp, Keppel Ltd (SGX: BN4 / FRA: KEP / KEP1 /OTCMKTS: KPELY / KPELF) has taken a completely different path.

While best known for aerospace and defense, Singapore Technologies Engineering Ltd (SGX: S63 / FRA: SJX / OTCMKTS: SGGKF) or ST Engineering has quietly emerged as a key player in Singapore’s smart-city transformation.

Sustained high interest rates over the last few years have impacted property developers negatively through higher financing costs and softer demand for properties.

With interest rates expected to trend lower, it might finally be time for them to shine.

CapitaLand Investment (CLI) — The Asset-Light Capital Manager

CapitaLand Investment Limited (SGX: 9CI), with its fee-driven model, provides investors with a defensive option for real estate exposure.

City Developments Limited (CDL) — The Hospitality & Residential Specialist

City Developments Limited (SGX: C09 / FRA: CDE / OTCMKTS: CDEVY) provides an option for investors seeking exposure to a traditional property developer.

UOL Group (UOL) — The Balanced All-Rounder

UOL Group Limited (SGX: U14 / FRA: U1O / OTCMKTS: UOLGY / UOLGF) offers a balanced mix of residential, commercial, and hospitality property exposure.

Change in classification by index provider set to bring in billions of dollars of investment

Thuy Anh Nguyen, a director at Dragon Capital, a Vietnamese fund manager, said the upgrade could potentially bring in tens of billions of dollars in active investment and around $500mn of passive inflows.

Wall Street and Asia had largely expected the EM upgrade, so the pop on the stock exchange will probably not be nosebleed. In any case, this is not exactly the MSCI Emerging Market Index, the gold standard for EM tracker funds.

The inclusions in MSCI EM will not take place until September 2026. The Vietnamese dong is under rising pressure in Southeast Asia’s most volatile FX market. Outflows from the VN index large caps have been as consistent as they are ominous. While the upgrade means a broader pool of foreign investors, the momentum in Vietnam after a solid rally is fading while the dong is, as always, a wild card.

Vietnam was the big gorilla in the frontiers market index with a 30% weight but its $350 billion stock market will be a pipsqueak relative to India and South Korea, Indonesia and China, the four Asian EM colossi.

Manufacturers in the country grapple with policy shifts and supply chain disruption

At Ather Energy Ltd (NSE: ATHERENERG / BOM: 544397)’s headquarters in traffic-clogged Bengaluru, an electronic map shows the company’s network of more than 4,000 charging points across India, along with real-time data from the touchscreen dashboards of its line of electric scooters.

The network is growing. Ather and other Indian electric scooter makers are preparing for millions of bike owners replacing petrol-powered rides with battery models, as charging infrastructure improves and vehicles become cheaper.

Powerful Indian conglomerate has suffered repeated crises in recent months

Two of Indian Prime Minister Narendra Modi’s top lieutenants have held an extraordinary meeting with executives from India’s Tata Group as one of the country’s most important conglomerates struggles to contain boardroom divisions and repeated crises among its businesses.

Kalyan Jewellers India Ltd (NSE: KALYANKJIL / BOM: 543278) is aggressively expanding its non-South presence and scaling its omni-channel platform, Candere, driven by an asset-light, franchisee-owned, company-operated (FOCO) model.

The FOCO model and a higher margin studded-jewellery mix in new markets are structurally improving return ratios and freeing up capital for aggressive, low-risk store rollouts.

With significant deleveraging and a clear path to enhanced profitability, the fundamental story remains intact, nudging investors to look beyond cyclical factors and towards execution consistency.

Strong recent credit off-take and a favorable interest rate environment for issuance are expected to drive a robust revenue quarter for CARE Ratings Ltd (NSE: CARERATING / BOM: 534804), building on its core debt rating services.

CareEdge’s focus on expanding its non-rating services, especially in ESG and infrastructure ratings, offers significant growth potential.

The Indian credit rating sector remains a high-margin oligopoly; a Q2 beat could re-rate CARE if it signals improved pricing discipline and acceleration in its non-rating advisory vertical.

Trent Ltd (NSE: TRENT / BOM: 500251) reported first half FY2026 revenue growth at 19%, well below the Street’s full-year consensus estimate of around 26%.

With Zudio store expansion wave now maturing and no new growth engine of comparable scale yet in sight, revenue growth appears to be normalizing to the low double-digit range.

In this context, the stock’s steep valuation multiples (78.5x 1-year forward P/E) look increasingly difficult to justify; as growth expectations are recalibrated a valuation de-rating seems likely.

Blue Star Ltd (NSE: BLUESTARCO / BOM: 500067)’s Q1 FY26 revenue grew by 4.1% YoY, with notable contributions from the B2B sector, international markets, and strong festive demand expectations despite unseasonal weather.

GST cuts and rising demand in healthcare, data centers, and commercial air conditioning drive growth, while strategic international expansion and R&D investments position Blue Star for sustainable success.

Blue Star remains a resilient player, leveraging strong B2B momentum, international expansion, and product innovation to navigate challenges and capitalize on future growth opportunities.

Info Edge (India) Ltd (NSE: NAUKRI / BOM: 532777) delivered 12.1% year-on-year growth in Q2 FY26 billings to INR 729 crore, led by steady momentum in Non-IT hiring and healthy traction in 99acres and Jeevansathi.

The mix shift toward Non-IT and consumer-facing platforms signals a stronger, more balanced growth profile, cushioning the business from the ongoing IT hiring slowdown.

With diversified revenue streams, disciplined cost control, and early benefits from AI integration, Info Edge appears positioned for sustained growth and gradual margin expansion ahead.

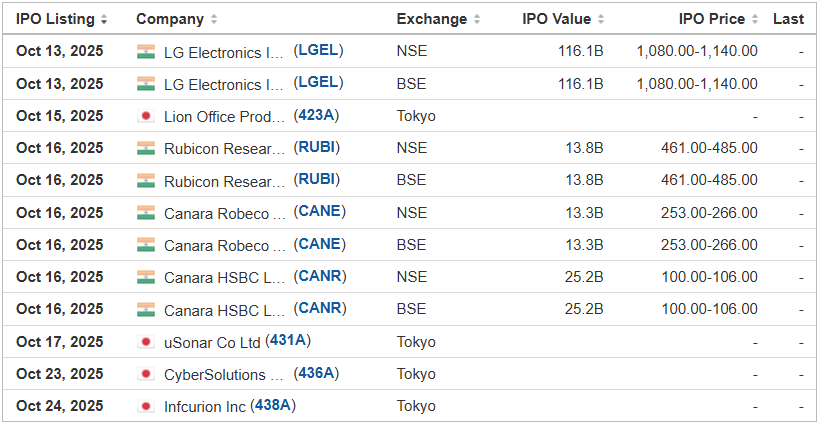

Indian listed markets have hitherto offered selective consumer appliance plays. LGEI will become the largest of them all, offering access to the structural growth of consumer appliances in India

IPO is priced attractively at 26-30x 1yr forward earnings. Near-term performance to benefit from recently announced indirect tax cuts as well as rate cuts. Must Apply

LG Electronics India’s USD 1.3 bn IPO, which opened on October 6, closes for subscription today, October 9, and is expected to list on October 14th.

LGEIL has secured Rs34.7 bn from anchor investors ahead of its Rs116.1 bn IPO, signaling a likely strong oversubscription at close today.

LGEIL IPO, priced at a steep discount to peers do not fully reflect company’s comparative strengths – strong market leadership, high returns and growth potential. Expect listing pop of 30%+.

There has an excellent demand for the LG Electronics India (LGEI) IPO among the institutional investors which sets the stage for a positive rally once it starts trading.

LGEI raised 4.43 trillion rupees in subscription funds during the general subscription period from 7 to 9 October. This amount is approximately 40 times the initial public offering (IPO) target.

Our base case valuation is target price of 1,514 INR which is 33% higher than the high end of the IPO price range.

With a PE of 7.2 and projected YOY revenue growth of 30%, Kaspi appears to be deep value. But, with geopolitical risks and currency devaluation, Kaspi could be too risky. Read on to see both sides:

KASPI (NASDAQ: KSPI / LON: 80TE / FRA: KKS) has quietly been one of the most underdiscussed fintech names in the past year but has recently seen a surge in recognition for its deep value potential. With Kaspi’s recent share price drawdown (down over 13% in the past month), their potential as an investment has come into question.

With earnings approaching in a month, the question of Kaspi’s quality as an investment now needs a timely answer. The bear and bull cases will both be presented here, and the reader will be able to decide for themselves which side is more compelling.

It has been a little over an year since I pitched KASPI (NASDAQ: KSPI / LON: 80TE / FRA: KKS) back in June 2024. The company listed on NASDAQ only in January 2024, and was relatively an unknown fintech operating out of Kazakhstan, a country that most of us still struggle to spell correctly. To a large extent, I think it is still an under the radar stock but not as obscure as it was an year back. Some of us who covered it back then realized it is similar to Tencent (HKG: 0700 / LON: 0LEA / FRA: NNND / SGX: HTCD / OTCMKTS: TCEHY). Now there are lot more substacks covering this stock. Since I pitched the deal has gotten much sweeter (Stock is down 33%), growth is de-risked (Expanding TAM) and the valuation much cheaper than earlier (7 times earnings).

The narrative is shifting. This former generics giant becomes a neuroscience growth story with a blockbuster catalyst—and why it’s still trading at a single-digit multiple.

Teva Pharmaceutical Industries Ltd (NYSE: TEVA) has quietly been one of the most interesting turnaround stories in healthcare. Once seen primarily as a debt-heavy generics giant, the company is now reshaping itself into a focused branded and specialty player with real momentum in neuroscience. Recent market activity underscores the shift: on October 2nd, the largest change in U.S. call options open interest was in Teva, where 35,000 contracts of October 2025 $21 calls were added. That kind of flow suggests institutional investors are positioning for upside over the next 12 months.

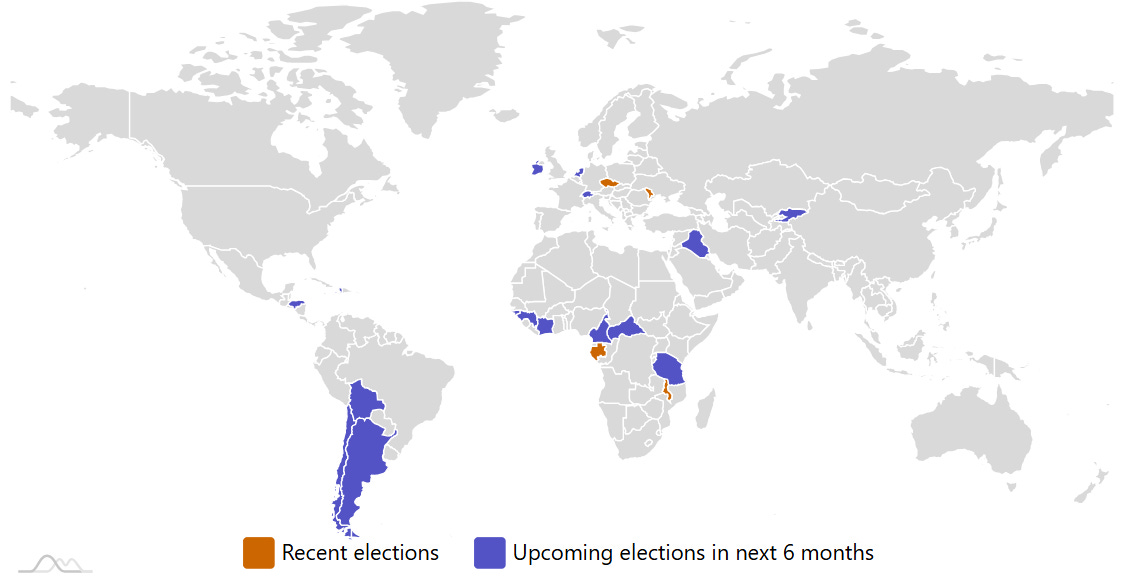

“Pink tide” among democracies may ebb in upcoming elections as voters in Chile, Colombia and Brazil shift to the right amid economic and immigration worries.

October LatAm Report: The Government Bonds Edition

Today’s article covers event-driven macro bets.

After more than a decade of populism and Marxism as the ruling philosophy in Latin America, the tide has turned to the right. Bukele in El Salvador and Milei in Argentina lead the change. I wager this is just the beginning of the regional shift to the right.

That said, the political calendar in LatAm is eventful for the next 12 months:

Bolivia: presidential runoff, October 19, 2025

Argentina: legislative election, October 26, 2025

Chile: presidential elections (first round), November 16, 2025

Chile: potential runoff December 14, 2025

Peru: presidential elections (first round), April 12, 2026

Colombia: presidential elections (first round), May 31, 2026

Brazil: presidential elections (first round), October 4, 2026

Deep Dive into MercadoLibre (NASDAQ: MELI): Valuation, Segment Growth, Key Metrics, GMV, TPV, Profitability, Expenses, Product Launches, Financial Stability, SBC/Revenue, and Shareholder Dilution.

MercadoLibre $MELI remains Latin America’s dominant e-commerce + fintech platform, compounding scale through Mercado Envios, Pago, and an expanding credit portfolio. Execution is visible in Q2 revenue +33.8% YoY, Argentina +77% YoY now 22% of revenue, and Mexico’s efficient scale via fulfillment and cross-border. Valuation looks appealing with Forward EV/Sales ~3.6 and Forward P/E ~40, supported by a durable moat, rising user growth, and improving short-term NPL trends. The setup favors long-term compounding. Read on.

Lessons from the climbers & scalers podcast — Part 2

Episodes 10–19 of the climbers & scalers podcast series reveal the most crucial phase of MercadoLibre (NASDAQ: MELI)’s journey, the transition from promising startup to global platform. These conversations highlight the strategic decisions and cultural principles that enabled MELI not only to survive multiple existential crises, but to emerge as the dominant force in Latin American commerce.

This is Part 2 of a three-part series on the climbers & scalers podcast. The final installment will cover MELI’s global expansion philosophy and long-term positioning.

The United States finalized a $20 billion lifeline for Argentina that will benefit Treasury Secretary Scott Bessent’s allies.

International investors have long looked at Argentina as a place to make a profit, particularly related to government debt that successive leaders have taken on. In many instances, investors are not the original bondholders, but have bought at a discount from the nation’s original lenders, and are wagering that the liens will eventually be repaid or renegotiated.

Adventures in the Chemicals Industry in Quest for Yield

Braskem SA (NYSE: BAK / BVMF: BRKM3 / BRKM5 / BRKM6) is often seen as a symbol of the chemical industry’s perceived death. The company’s shares are trading at multidecade lows, and its fixed income could be acquired at a massive discount to par.

Chemical producers such as Braskem are an illustration of how easily we love to ignore the old economy. Yet, we forget that the physical reality is built on four pillars: cement, steel, ammonia, and plastics. In other words, the chemical industry is one of the core industries for our material world.

On 24 February 2025, Nu Holdings (NYSE: NU) released a video on their YouTube channel where the CEO, David Velez, said the following:

“2025 will be the year when we finally start making the first significant steps towards going beyond Latin America and thinking of the world where Nu is more of a multi-country, multi-region, multi-continental technology company.”

Today, Nu began those first steps of going beyond Latin America by applying for a banking charter in the US!

This is a massive announcement on which the stock should have been up 20%, however, it is flat, likely due to the upcoming US government shutdown.

Let’s analyze this announcement and the implications for Nu.

Chilean stocks rallied 30% in 2025 and should do even better in 2026.

Summary

Chilean equities, especially Banco de Chile (NYSE: BCH), are poised to rally as conservative candidate Jose Antonio Kast is overwhelmingly favored to win the presidency.

Current polling misleads foreign investors; right-wing candidates collectively have a huge lead which will become apparent after November’s first round vote.

A Kast presidency, combined with high commodity prices, sets the stage for 5%+ annualized GDP growth and outsized equity returns.

Banco de Chile is my favorite way to express this trade.

Also: other U.S.-listed Chilean stocks, the Nuam exchange, and betting on the election results outright.

🌐 Nebius Group NV (NASDAQ: NBIS) – AI-centric cloud platform built for intensive AI workloads. Sold Yandex to a consortium of Russian investors. Retains several businesses outside of Russia. 🇼🏷️

Note: Investing.com has a full calendar for most global stock exchanges BUT you may need an Investing.com account, then hit “Filter,” and select the countries you wish to see company earnings from. Otherwise, purple (below) are upcoming earnings for US listed international stocks (Finviz.com):

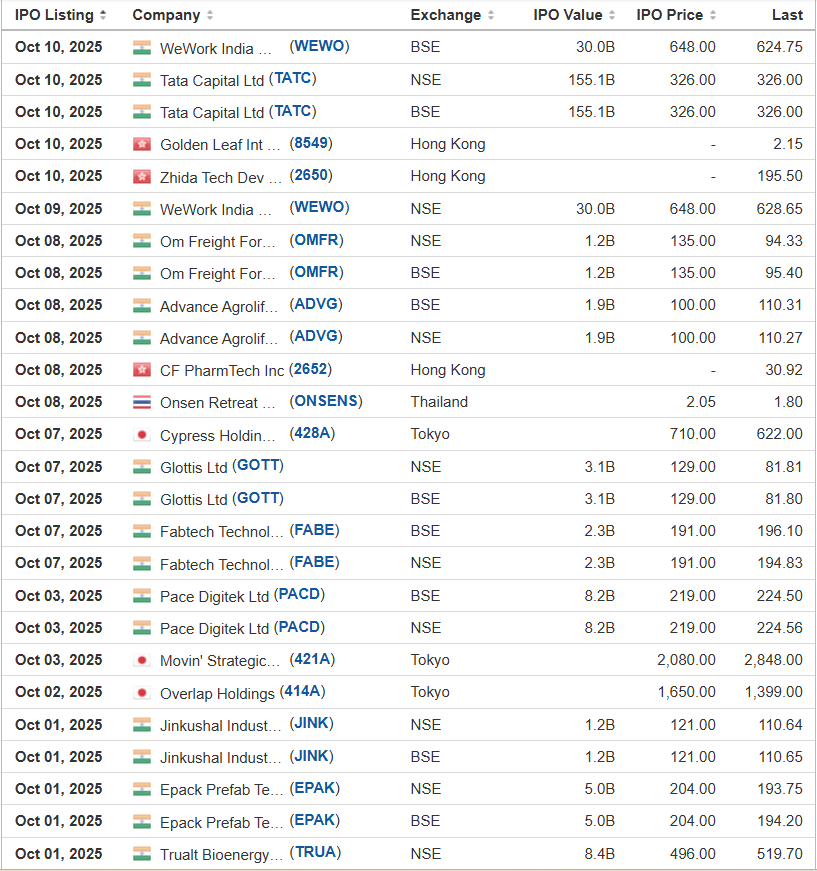

Frontier and emerging market highlights from IPOScoop.com and Investing.com (NOTE: For the latter, you need to go to Filter and “Select All” countries to see IPOs on non-USA exchanges):

Note: Leifras is offering American Depositary Shares (ADS) in its IPO. Each ADS represents one ordinary share.

Headquartered in Shibuya-ku, Tokyo, we are a sports and social business company dedicated to youth sports and community engagement. We primarily provide services related to the organization and operations of sports schools and sports events for children. Building upon our experience and know-how in sports education, we also operate a robust social business sector, dispatching sports coaches to meet various community needs.

At the core of our operations is the children’s sports school business. When we refer to a sports school, it refers to a series of courses and programs that we offer to teach a sport, instead of a physical location. As of December 31, 2024, we were recognized as one of Japan’s largest operators of children’s sports schools in terms of both membership and facilities. As of the date of this prospectus, we hold our sports classes at more than 4,500 facility locations in Japan nationwide, serving over 62,400 members. The number of members is based on the number of students taking classes; if a student is enrolled in two different classes, this student is counted as two members. We provide 13 sports schools, from soccer school “Liberta” and basketball school “Porte,” to rhythmic karate school “Quore” and kendo school “Kokoro.”

We also offer classes that cater to the various needs of different age groups and sports capability levels. For instance, our “JJMIX” classes offer beginners from the age of 2 and up, the opportunity to experience multiple sports, and our “Rugina” classes are designed specifically for girls. Approximately 87 percent of our sports school members are elementary school students, with additional programs for preschoolers, nursery school children, kindergarteners, and junior high school students. These classes are taught by professional coaches who bring their expertise and passion to each session, ensuring that students receive high-quality coaching in safe environments. Our sports school business also extends to sports merchandise sales and commissioned special guidance services.

Our approach to sports education emphasizes the development of non-cognitive skills, which are crucial for success both inside and outside the sports arena. Following our teaching principle “acknowledge, praise, encourage, and motivate,” our classes integrate non-cognitive skills, such as motivation, teamwork, strategic thinking, and sportsmanship, into our sports curriculum. For instance, our soccer program focuses on developing technical skills, tactical understanding, and teamwork, and our martial arts programs in karate and kendo promote physical fitness and self-discipline. Our holistic approach integrates physical and mental development, setting us apart in the industry.

Building upon our experience and know-how in sports education, our social business mainly dispatches sports coaches to meet various community needs. Our school club support business provides sports coaching in school club activities and physical education classes and coordinates collaborations between school clubs and private companies. Our LEIF after-school daycare service supports children with disabilities or developmental characteristics through soccer therapy, promoting independence and improving life skills.

Our involvement also extends to facility management services at public sports facilities, focusing on providing sports coaching for people of all ages. Our elderly healthcare initiative offers exercise programs for the elderly, including exercise instruction such as preventive nursing care exercises, yoga, and other health promotion services at community centers and healthcare facilities. By addressing these diverse needs, we aim to promote physical health, social inclusion, and community well-being across different demographics.

Note: Net income and revenue are for the fiscal year that ended Dec. 31, 2024.

(Note: Leifras Co., Ltd. priced its IPO at $4.00 – the low end of its price range – and sold 1.25 million shares – the number of shares in the prospectus – to raise $5.0 million. Background: Leifras Co., Ltd. cut its IPO’s size to 1.25 million shares – down from 1.6 million shares initially – and kept the price range at $4.00 to $5.00 to raise $5.63 million, if priced at the mid-point of its range, according to its F-1/A filing dated May 20, 2025. Leifras, however, said in the prospectus that the assumed IPO price is $5.00 – and at that price – the IPO would raise $6.25 million. Background: Leifras Co., Ltd. filed its F-1 on Dec. 10, 2024, and its original IPO terms called for 1.6 million shares at a price range of $4.00 to $5.00 to raise $7.2 million.)

We conduct our business through the VIEs, Yoda Metal and DL Metal, in the Philippines. We primarily engage in recycling, production and trading of recycled scrap metals in the Philippines.

We are a waste materials and scrap metal recycling company in the Philippines. Our capabilities are underscored by our permitted capacity for metal recycling, measured in tons per year, and by the government-issued license that enables us to import hazardous waste (as raw materials) into the Philippines. We process raw materials and generate final products that include copper alloy ingot, aluminum scrapes, plastic beads, and others. We provide economical and flexible solutions to the challenges of electronic waste, metal scrap and industrial recycling. By providing lower-cost alternatives for processing recycled materials, we not only contribute to environmental sustainability but also highlight our role as a modern and specialized recycling company.

We have established an environmentally friendly technology that we believe sets us apart from competitors. Our exhaust gas recirculation system and exhaust emissions have been examined and approved annually by the Environmental Management Bureau (“EMB”) in the Philippines. Our exhaust gas recirculation system enhances process efficiency while minimizing and, in some cases, eliminating contamination. Through this system, we capture the ash and slag contained in the emissions for further metal recovery ad smelting, ensuring the exhaust we ultimately release meets all applicable standards. In contrast, competing technologies, such as table concentrators, cannot prevent pollution during the final stages of processing.

Due to our sustainable, environmentally friendly processes, we believe we are well-positioned to comply with heightened regulations across the globe.

We benefit from being fully authorized by the government to process hazardous wastes under the framework of The Basel Convention: A Global Solution for Controlling Hazardous Wastes.

We have complied with all governmental documentary requirements, including Environmental Compliance Certificate (the “ECC”), Permit to Operate, Discharge Permit, Import and Export Permit. As of December 31, 2024, our workforce consisted of 97 employees, including 7 engineers. Electronic waste and metal scraps from local and abroad (Korea, Japan, Southeast Asia, Europe, USA, etc.) are carefully segregated and processed in compliance with the existing environmental laws, rules and regulations. Our annual processing capacity is estimated to be around 300,000 tons.

Investors in our Class A Ordinary Shares should be aware that they are purchasing equity in One and one Cayman, which does not directly own our business in the Philippines. Please refer to the information contained in and incorporated by reference under the heading “Risks Related to Our Corporate Structure” on page 19 of this prospectus.

Note: Net income and revenue are in U.S. dollars for the year that ended Dec. 31, 2024.

(Note: One and One Green Technologies Inc. trimmed its small IPO at pricing to 2.0 million shares – down from 2.5 million shares in the prospectus – and priced the IPO at $5.00 – the mid-point of its range – to raise $10 million on Wednesday night, Oct. 8, 2025. Background: One and One Green Technologies was offering 2.5 million shares at a price range of $4.00 to $6.00 to raise $12.5 million, if priced at the $5.00 mid-point of its range, according to its F-1/A filings.)

(Note: In June, Cathay Securities was named the sole book-runner, replacing The Benchmark Company and Axios Capital, the original team of joint book-runners, according to One & One Green Technologies’ F-1/A filing dated June 6, 2025.)

OBOOK Holdings (Direct Listing)OWLS D. Boral Capital (ex-EF Hutton) (Financial Adviser), 4.7M Shares, 0.00-0.00, $0.0 mil, 10/13/2025 Week of

Note: This is NOT an IPO. This is a Direct Listing on the NASDAQ. D. Boral Capital will serve as the financial adviser. Existing shareholders will sell stock in the direct listing. No new stock will be issued and/or sold, according to the prospectus..

The company’s operating entity, OwlTing Group, runs blockchain-driven service platforms for companies in a variety of industries:

OBOOK – for e-commerce, hospitality and payments – for companies and people involved in cross-border transactions;

OwlPay – for payment products and services

OwlNest – for hospitality products and services

OwlTing Market – for an e-commerce platform and services.

Note: Net loss and revenue are in U.S. dollars for the 12 months that ended Dec. 31, 2024.

(Note: OBOOK Holdings’ shareholders will sell up to 4.73 million shares (4,729,695 shares) of stock in the NASDAQ Direct Listing, according to an F-1/A filing dated Sept. 19, 2025. No reference price has been set yet. In 2025, OBOOK Holdings said its stock sold for $10.00 per share in a private placement, according to the prospectus.)

UltratrexUTX Craft Capital Management, 1.3M Shares, $4.00-6.00, $6.3 mil, 10/13/2025 Week of

(Incorporated in the Cayman Islands)

We make marine environmental cleanup and dredging machinery.

We provide environmental solutions that rely on amphibious machinery, aquatic weed harvesters and dredgers.

Environmental cleanup projects, habitat restoration and land reclamation make up most of our projects. We serve customers mostly in Southeast Asia, the Middle East and some parts of Europe.

Note: Net income and revenue are in U.S. dollars for the 12 months that ended on Dec. 31, 2024.

(Note: Ultratrex is offering 1.25 million shares at a price range of $4.00 to $6.00 to raise $6.25 million, according to its F-1/A filings.)

Altech Digital Co., Ltd.ALD Pacific Century Securities/Revere Securities, 1.5M Shares, $4.00-4.00, $6.0 mil, 10/15/2025 Week of

(Incorporated in the Cayman Islands)

We offer IT system development, maintenance and consulting services in Hong Kong.

Altech Hong Kong, our operating subsidiary, offers two types of IT services: system development services, which include developing web-based systems and mobile applications, as well as maintenance and consultancy services for these systems after development.

Note: Net income and revenue are in U.S. dollars for the year that ended March 31, 2025.

(Note: Altech Digital Co., Ltd. is offering 1.5 million shares at the assumed IPO price of $4.00 to raise $6.0 million, according to its F-1/A filings.)

We are the first company in Japan to obtain a license plate number for imported electric light commercial vehicles. We are the second company and also one of the three companies that sell electric light commercial vehicles in Japan as of the date of this prospectus. (Incorporated in Japan)

The electric light commercial vehicles we sell belong to the category of “light commercial vehicles,” which are commercial carrier vehicles with a gross vehicle weight of no more than 3,500 kilograms.

We commenced selling and delivering two models of electric light commercial vehicles, ELEMO and ELEMO-K, in Japan in April 2022 and July 2022, respectively, and have been working with Cenntro, our cooperating manufacturer, to produce them under our brand, “ELEMO,” in its factory in Hangzhou, China. ELEMO is the first electric vehicle we sell and (it) is the second electric light commercial vehicle that has ever been sold in Japan since the commencement of sales of MINICAB-MiEV in December 2011, which was the first electric light commercial vehicle produced by Mitsubishi Motors Corporation. Since June 2023, we have commenced the sales of a new model called “ELEMO-L,” a van-type electric vehicle that could be used for commercial and recreational camping purposes, which we expect may enable us to increase consumer market penetration.

Under our Exclusive Basic Transaction Agreement dated March 31, 2021 with Cenntro (the “Exclusive Basic Transaction Agreement”), Cenntro manufactures ELEMO, ELEMO-K, ELEMO-L, and other electric vehicles under the specifications designated by us in their manufacturing factories in China and delivers the electric vehicles to the ports in China designated in the individual agreement for a particular order. We arrange for the shipment from these ports to the Port of Yokohama or other designated ports in Japan. Upon arrival, we transport the vehicles to our research laboratory located in Chiba, Japan, for inspection, and then send them to our business partners’ facilities, Anest Iwata’s factory in Fukushima, Japan, and TONOX’s factories in Kanagawa, Japan. The specialists of Anest Iwata, a Tokyo Stock Exchange-listed company that specializes in industrial machinery, supplies, and components, and TONOX, a Japanese commercial vehicle manufacturer, modify the vehicles to comply with the regulations and standards for the Japanese market, install the accessories, and undertake the inspection in accordance with our instructions. After the inspection and modifications, we deliver the electric vehicles to the governmental vehicle inspection office, the National Agency for Automotive and Land Transportation Technology, for individual imported vehicle inspection, and the local land transportation office for registration. Upon completion of the individual imported vehicle inspection and registration, we conduct the final inspection in our research laboratory located in Chiba, Japan, and deliver the electric light commercial vehicles to the customers.

Since the inception of our operation, we have been leveraging the customizability and adjustability of our electric light commercial vehicles to attract corporations in different industries and local governments that have varying needs from their departments in Japan. During the fiscal years ended September 30, 2023 and 2022, we sold and delivered 52 and 16 electric light commercial vehicles to 14 and 11 customers, respectively.

Note: Net loss and revenue figures are in U.S. dollars (converted from Japanese yen) for the fiscal year that ended Sept. 30, 2024.

(Note – New IPO Plans: HW Electro Co., Ltd. filed an F-1 dated May 8, 2025 – the same date that it withdrew its previous IPO plans in a letter to the SEC. In the new IPO document – the F-1 dated May 8, 2025 – HW Electro Co., Ltd. disclosed that it is offering 4.15 million American Depositary Shares (ADS) at an assumed IPO price of $4.00 to raise $16.6 million. American Trust Investment Services and WestPark Capital are the joint book-runners.)

(Background on Previous IPO plans: Registration Withdrawn on May 8, 2025 – A.C. Sunshine and Univest Securities were the joint book-runners. Note: HW Electro Co., Ltd. filed an F-1MEF to increase its IPO’s size at pricing by 200,000 shares, according to a filing dated Jan. 24, 2025. Note: HW Electro Co., Ltd. filed an F-1/A to increase its IPO’s size to 4.0 million ADS – up from 3.75 million ADS – and increase the assumed IPO price to $4.00 – up from $3.00 – to raise $16.0 million – up from $11.25 million initially – according to an F-1/A filing dated Dec. 23, 2024. In that same filing, AC Sunshine Securities was added as the lead left joint book-runner to work with Univest Securities as the other joint book-runner, and the IPO’s proposed venue was changed to the NASDAQ from the NYSE – American Exchange, with the proposed symbol changed to “HWEP” from “HWEC”. Note: HW Electro Co., Ltd. filed its new F-1 (prospectus) on April 26, 2024, disclosing plans for its IPO and its listing of American Depositary Shares (ADS) on the NYSE – American Exchange: 3.75 million ADS at an assumed IPO price of $3.00 per ADS. Each ADS represents one ordinary share. Background: HW Electro Co., Ltd. withdrew its previous IPO plans that called for a listing on the NASDAQ with a different proposed symbol.)

Smart Logistics Global Ltd.SLGB Craft Capital Management/Revere Securities, 1.0M Shares, $5.00-6.00, $5.5 mil, 10/15/2025 Week of

We are a holding company whose operating subsidiary in China manages a business-to-business logistics provider, focused on the transportation of industrial raw materials. (Incorporated in the Cayman Islands)

Note: Net income and revenue are in U.S. dollars for the 12 months that ended Dec. 31, 2024.

(Note: Smart Logistics Global Ltd. filed an F-1/A dated Aug. 20, 2025, in which it named Craft Capital Management as the new lead left underwriter, to work with Revere Securities. Smart Logistics Global Ltd. is offering 1.0 million shares at a price range of $5.00 to $6.00 to raise $5.5 million.)

(Background: Smart Logistics Global Ltd. withdrew its original IPO plans in a letter to the SEC on July 14, 2025, because more than six months had elapsed since the company had updated its IPO filing. On that same date – July 14, 2025 – Smart Logistics Global Ltd. refiled its IPO plans – same terms as the original prospectus with 1 million shares at a price range of $5.00 to $6.00 – and the disclosure of a new sole book-runner, Revere Securities, to replace the previous underwriting team of Benjamin Securities and Prime Number Capital.)

(More Background: Smart Logistics Global Ltd. filed an F-1/A dated Dec. 6, 2024, and updated its financial statements through the period ending June 30, 2024. Background: Smart Logistics Global Ltd. filed an F-1/A dated Nov. 20, 2024, and disclosed the terms of its IPO: The company is offering 1 million shares at a price range of $5.00 to $6.00 to raise $5.5 million. Background: Smart Logistics Global Ltd. filed its F-1 for its IPO on Oct. 4, 2024, with estimated IPO proceeds of $10 million.)

Agencia Comercial SpiritsAGCC D. Boral Capital (ex-EF Hutton)/Revere Securities, 1.8M Shares, $4.00-6.00, $9.0 mil, 10/17/2025 Friday

(Incorporated in the Cayman Islands)

We are a whisky retailer and distributor based in Taichung City, Taiwan.

We are committed to offering imported whisky of world-class quality to our clients. Agencia Taiwan has grown rapidly since its inception, leveraging its extensive industry experience, strategic partnerships and innovative business model to establish itself as a trusted and prominent player in the whisky market. Our mission is to enhance the whisky experience in Taiwan and other Asia-Pacific countries by offering expert guidance, competitive pricing and exceptional customer service.

Our Group operates across three primary business areas:

• Bottled Whisky Sales: Sourcing bottled whisky from local suppliers in Taiwan and reputable distilleries in the UK, the company, along with its downstream distributors, sells these products to bars, restaurants, nightclubs, VIP lounges and corporate clients.

• Raw Cask Whisky Sales: Starting in 2023, our group expanded into the procurement and sale of raw cask whisky sourced directly from distilleries in the UK. These unprocessed casks are sold directly to other liquor and spirits distributors, enabling our Group to tap into a broader market segment.

• Cask-to-bottle and distribution business: Beginning in 2025, our Group ventured into the cask-to-bottle and distribution business, which involves brand-authorized whiskey bottling, packaging and sales. Under this model, it obtains brand licenses, sources raw cask whisky directly from brand owners, and conducts bottling and packaging in Taiwan with the aid of local contract manufacturers.

From 2020 to now, our development can be divided into the following stages:

• Start-up period (2020-2022): During its initial years, our Group primarily focused on bottled whisky sales, following a business-to-business (B2B) model. By sourcing both locally and internationally, our Operating Subsidiary developed a network of suppliers and clients.

• Growth period (2023-2024): Our Group expanded its operations to include the sale of raw cask whisky sourced directly from distilleries, accounting for a significant portion of its revenue. This diversification allowed it to offer unique high-quality products while continuing to focus on B2B relationships.

• Expansion in 2025 and Beyond: Our Group plans to expand its operations to include collaboration with brand owners. This will involve obtaining brand authorization through the payment of licensing royalties, sourcing raw cask whiskey from these brand owners, and conducting bottling and packaging in Taiwan, primarily through local contract manufacturers, for which processing fees will be incurred. Our Group will then market and sell products under the respective brands. Initially, the primary customers will be distributors, focusing predominantly on a business-to-business model.

“From Barrel to Bottle” represents our Group’s core value, highlighting its dedication to delivering a comprehensive one-stop whiskey distribution service. Our Group provides an extensive range of products and utilizes a diverse array of sales channels. Consequently, both business volume and profit have experienced average annual growth. Our distribution channels encompass a broad swath of Taiwan, including clubs, restaurants, bars, hotels, VIP lounges, and corporate clients through our downstream distributors. Looking ahead, we aim to further diversify our product offerings, expand its footprint in the Asia-Pacific region, and solidify our position as a trusted key whisky distributor. By combining our client-centric approach, strategic partnerships, and focus on premium products, we believe that we are well-positioned to capture a significant share of the growing demand for high-quality whiskey in Asia and beyond.

Note: Net income and revenue are for the 12 months that ended Dec. 31, 2024.

(Note: Agencia Comercial Spirits filed its F-1 on July 10, 2025, and disclosed the terms for its IPO: 1.75 million shares at a price range of $4.00 to $6.00 to raise $9.0 million, if priced at the $5.00 mid-point of its range.)

ELC Group Holdings Ltd.ELCG D. Boral Capital (ex-EF Hutton), 1.9M Shares, $4.00-6.00, $9.4 mil, 10/17/2025 Friday

(Incorporated in the Cayman Islands)

We are a manpower service provider based in Singapore. Manpower service providers (“MSP”) serve as a bridge between job seekers and businesses to meet each other’s recruitment needs. Typically, MSPs create a platform whereby employers can list job opportunities and recruit individuals looking to secure full, temporary or part-time employment meeting their respective criteria. For companies, MSPs assist the recruitment process to meet particular staffing needs, saving companies time, money, and effort. For job seekers, MSPs help them find an appropriate job matching their skill sets as quickly as possible, and exposing them to more opportunities through their vast network.

Our customers fall into a wide range of industries, including warehouse and logistics, food and beverage, cleaning, manufacturing, retail and events. To provide better service to our customers, we pay close attention to the changing needs of our customers, including new developments in their respective industries, which helps us anticipate the specific roles and skills that they will need. We believe this attention to detail gives us a significant competitive advantage and improves customer loyalty.

We have developed a proprietary platform that connects job seekers and employers through a unique matching program using specific character and skill recognition matrices. Our platform operates a comprehensive database that records the skill preferences and requisite applicant characteristics of our business customers and the job criteria of job seekers, thereby reducing reliance on subjective human analysis which can be extremely time consuming and inefficient. While many MSPs offer similar services, we believe our model is more specifically focused on our customers’ individual criteria, therefore we tend to deliver a more tailored approach, rather than providing a one-size-fits-all service.

Job Seekers – We believe we stand out to job seekers in two important ways: (i) we have developed a mobile app to enable clients real-time access to the data and therefore opportunities, and (ii) we are the first manpower provision company operating with an app platform in Singapore that is compensating part-time workers on the very same day they finish their jobs.

We have artificial intelligence (“AI”) technology integrated into our “EL Connect App” to create a positive user-friendly experience for part-time job seekers.

Employers – For employers, in addition to the EL Connect App, we have also developed our “Taskforce App.” Our TaskForce App is a smart platform to digitalize building and property operations management. Our TaskForce App integrates internet of things (“IoT”) sensors, facial recognition systems and robotics into facilities and workforce management in buildings and properties. TaskForce App bridges the gap between the employees of our customers, such as site supervisors who oversee property management, and contractors or crews of our customers, who perform individual duties and tasks, addressing inefficiencies in traditional and paper-based processes of property management. Our TaskForce App seeks to achieve optimal performance and productivity for our customers by enabling their employees to have real-time monitoring of facilities and workforce management and providing them instant access to a variety of information ranging from attendance records of contractors or crews to real-time usage of consumable supplies in a facility. This has become an invaluable tool to our customers which has prompted us to monetize its application by opening it up to customer subscriptions and licensing, which we expect will become a growing revenue stream.

We derive our revenue primarily from the following sources: (i) manpower supply services – which provides part-time manpower to customers on our employment and recruitment portal “EL Connect Mobile”; (ii) manpower contracting services – which provides cleaners for cleaning services; (iii) software as a service (“SaaS”) sales, which grants users the right to access our “Taskforce” app; (iv) software licensing sales, which grants clients the right to use the Taskforce app customized to their specific requests (updates and maintenance included); and (v) project management services.

Note: Net income and revenue are in U.S. dollars for the 12 months that ended Dec. 31, 2024.

(Note: ELC Group Holdings Ltd. increased its IPO’s size again – this time to 1.87 million shares – up from 1.7 million shares – and kept the price range modest at $4.00 to $6.00 – to raise $9.35 million, according to an F-1/A filing dated Aug. 25, 2025.)

(Note: ELC Group Holdings Ltd. raised the size of its IPO to 1.7 million shares – up from 1.25 million shares originally – and kept the price range at $4.00 to $6.00 – to raise $8.5 million. Background: ELC Group Holdings Ltd. disclosed the terms for its small IPO – 1.25 million shares at a price range of $4.00 to $6.00 – to raise $6.25 million, if priced at the $5.00 mid-point of its range, according to an F-1/A filing dated June 27, 2025. Initial Filing: ELC Group Holdings Ltd. filed its F-1 on March 4, 2025.)

Libera Gaming OperationsLBRJ D. Boral Capital (ex-EF Hutton)/Craft Capital Management/ Boustead Securities, 1.3M Shares, $4.00-4.00, $5.0 mil, 10/20/2025 Week of

We operate 11 pachinko gaming halls in Japan, as of March 15, 2024. (Incorporated in Japan)

We are a large and growing pachinko hall operator in Japan. Libera Gaming Operations, Inc. was founded in Japan in May 1965 and has been operating pachinko halls for over 58 years. Pachinko halls provide a venue for customers to play two types of recreational arcade games: “pachinko” and “pachislot,” which are played using pachinko balls and pachislot tokens, respectively, for the purpose of obtaining more balls and tokens and exchanging them for prizes. Customers can convert some prizes into cash by having independent buyers from pachinko halls buy them. The pachinko and pachislot industry is highly regulated under Japanese laws and regulations. Playing pachinko and pachislot machines are not considered a form of gambling in Japan because customers do not directly win cash. They win tokens that may be redeemed for prizes, which in turn may be sold for cash by independent buyers. We have over 58 years of experience in the pachinko industry, operating eleven pachinko halls in Japan as of March 15, 2024. There are only 161 pachinko hall operators that operate more than ten pachinko halls out of a total of 1,623 operators in Japan as of 2023, and we are one of the largest pachinko hall operators as we are in top 10% of all pachinko hall operators with respect to the number pachinko halls operated (Source: “Pachinko hall operator survey 2023”, Yano Research Institute). For the years ended October 31, 2023 and 2022, with respect to our pachinko operation business, we reported total revenues of ¥4,874,215 thousand (US$32,182 thousand) and ¥3,966,010 thousand, respectively.

We also operate a real estate business, in which we conduct real estate redevelopment, property rental and property brokerage. We focus our real estate business in the central Tokyo area, where we use our experience and our network of real estate brokers gained through our pachinko and pachislot business to determine investment decisions with a goal of maintaining a profitable real estate business. Our main source of real estate revenue is from real estate redevelopment. We purchase old real estate in the central Tokyo area where we expect increasing demand in the future and we believe rents and asset values are unlikely to decline, and we redevelop and renovate the properties by using third party contractors with a goal to generate higher rental revenue. We believe the central Tokyo area has many prospective buyers, and therefore we believe that we can sell the real estate and generate a high profit in a short period of time. In addition, since we have historically purchased real estate for redevelopment purposes in what we consider good locations close to train stations in the city center, we believe we can generate rental revenue during the period between our purchase of the properties until we begin redevelopment. During the year ended October 31, 2023 we generated ¥980,543 thousand (US$6,474 thousand) from the sale of one property and during the year ended October 31, 2022 we generated ¥3,705,626 thousand from the sale of two properties. We believe that the real estate market in Tokyo is relatively cheaper than other international cities, and as such we expect that more investors will be attracted to property in Tokyo and the real estate market will continue to grow in the future.

For the years ended October 31, 2023 and 2022, we reported total revenues of ¥6,106,306 thousand (US$40,317 thousand) and ¥7,906,120 thousand, respectively, net income of ¥557,802 thousand (US$3,685 thousand) and ¥200,185 thousand, respectively, and net cash provided by operating activities of ¥3,203,829 thousand (US$21,153 thousand) and ¥5,257,783 thousand, respectively, on a consolidated basis. As noted in our audited consolidated financial statements, as of October 31, 2023, we had retained earnings of ¥10,375,305 thousand (US$68,502 thousand). As noted in our audited consolidated financial statements, as of October 31, 2023, we had total liabilities of ¥17,769,154 thousand (US$117,319 thousand).

Note: Net income and revenue are in U.S. dollars (converted from the Japanese yen) for the fiscal year that ended Oct. 31, 2023.

(Note: Libera Gaming Operations said it has applied to the NASDAQ as its listing venue, according to a Free Writing Prospectus dated Sept. 18, 2024, for its micro IPO – just 1.25 million shares at $4.00 – the low end of its $4.00-to-$6.00 price range – to raise $5.0 million. Background: Libera Gaming Operations increased the number of shares in its IPO to 1.25 million shares – up from 1.0 million – and cut the price range to $4.00 to $6.00 – down from $5.00 to $7.00 previously – to raise $6.0 million, assuming that the IPO will be priced at $4.00, the low end of its new range, according to an F-1/A filing dated Sept. 16, 2024. Background: Libera Gaming Operations said in a June 26, 2023, filing that it intends to apply to the NYSE – American Exchange to list its stock. The company has already applied to the NASDAQ to list its stock.)

We run English learning centers for children in Hong Kong.

We offer children’s language classes – mostly in English – and some in Mandarin. We serve students ages 3 to 14 through our 20 learning centers in Hong Kong that offer classes in phonics, reading, grammar, writing, conversation and preparation for exams.

We have licensed the “Monkey Tree” brand to other operators that run another 38 centers in Hong Kong.

(Note: Monkey Tree Investment Ltd. disclosed its IPO terms on Aug. 15, 2025, in an F-1 filing: The company is offering 1.6 million shares at a price range of $4.00 to $5.00 to raise $7.0 million, according to its F-1 filing dated Aug. 15, 2025.)

Bgin Blockchain Ltd.BGIN D. Boral Capital (ex-EF Hutton), 6.0M Shares, $5.00-7.00, $36.0 mil, 10/21/2025 Tuesday

We make cryptocurrency mining equipment. Our focus is on alternative currencies. (Incorporated in the Cayman Islands)

Through our operating subsidiaries, we are a digital asset technology company based in Singapore, Hong Kong, and the U.S. with proprietary cryptocurrency-mining technologies and a strategic focus on alternative cryptocurrencies.

For the fiscal year ended December 31, 2022, we generated substantially all of our revenue from cryptocurrency mining. Since April 2023, we have generated revenue from selling mining machines designed by us, and sales of mining machines contributed approximately 85.43% and 65.71% of our total revenue for the fiscal year ended December 31, 2023, and the six months ended June 30, 2024, respectively.

Our subsidiaries design and sell mining machines equipped with our proprietary 8nm or 12nm ASIC chips under different series dedicated to the mining of KAS coins, ALPH coins, RXD coins, and ALEO coins. These machines are available for purchase only through our website, iceriver.io. Customers may view and place orders for machines they intend to purchase directly through the website, and have the option to enroll in our miner hosting services, through which we operate and manage mining machines on customers’ behalf in return for service fees. Customers purchasing machines sold by our subsidiaries are primarily based in Hong Kong, the U.S. and Southeast Asia. For the fiscal year ended December 31, 2023, and the six months ended June 30, 2024, we sold an aggregate of 67,998 and 47,252 mining machines, respectively, to customers across the world. As of the date of this prospectus, we host a total of 4,020 machines on behalf of our customers, of which 2,969 are in operation at our mining farm located in York, Nebraska, and a hosting facility in Coon Rapids, Iowa, and 1,051 are stored in our warehouse in Beatrice, Nebraska.