Emerging Market Links + The Week Ahead (May 20, 2024)

by

We covered Starbucks a few weeks ago where I suspected some of their troubles in China are due to the rapid expansion of bubble tea chains plus a new standalone coffee chain attached to existing KFCs. Momentum Works has a podcast discussing the troubles Luckin (OTCMKTS: LKNCY),who was the subject of a major accounting scandal and delisted from the NASDAQ some years ago, might be giving them in the Chinese coffee market.

I had also noted Starbucks is the subject of boycotts in Muslim countries like Malaysia, Indonesia, etc. over Gaza. Homegrown Malaysian coffee chain ZUS Coffee, who’s goal is to become the largest coffee chain in Malaysia, served coffee at a recent Adidas event which they posted about on Instagram. They were instantly subjected to a boycott campaign for doing so (as Adidas is apparently on the BDS boycott list although I can’t seem to find a full updated list anywhere…) and then for not mentioning Palestine in their first apology statement:

I don’t know how much attention boycotts of Western businesses are getting in Western corporate media, but clearly business executives and investors need to start paying attention to them as they will eventually start hitting bottom lines…

Finally, Lula has ousted Petrobras’ CEO as he needs them to invest more in Brazil to juice up its sagging economy – not pay juicy dividends to foreign investors. Frankly, there is just too much political drama surrounding the stock (albeit its a favorite of Seeking Alpha writers just for that reason) – there are other state-owned oil companies that come with less drama and good dividends.

The Petrobras saga reminds of what happened with Petronas some years ago when Malaysia’s politicians abruptly changed the state-owned company’s strategic direction from heavily investing overseas to focus more on investing at home (to help shore up the sagging political fortunes of the ruling party at the time…).

A Western expat (one of the many expensive expats they had hired to drive international expansion who got laid off) had explained to me that Petronas’ purpose was nation building (aka provide a dividend to the government and no doubt the Provident Fund). So while investing overseas made sense from a business standpoint (diversification…), it went against the company’s mission statement and purpose (nation building…) plus all the overseas investing (and the hiring of expensive Western expats…) was not easy to explain to increasingly unhappy voters at home…

A look at all 122 stock holdings of the iShares MSCI Taiwan ETF (NYSEARCA: EWT) + Franklin FTSE Taiwan ETF (NYSEARCA: FLTW) + their performance along with that of The Taiwan Fund, Inc (NYSE: TWN).

Understanding the AI supply chain in Asia, growth drivers in Asia, why commercially experienced & skilled directors are valuable, growing EM dividends, why & where of EM, new April factsheets, etc.

Investors of Li Auto (NASDAQ: LI)’s Nasdaq-listed shares filed a class action lawsuit against the Chinese electric vehicle (EV) maker in the United States, alleging it inflated market demand for the Li Mega multi-purpose vehicle (MPV) when it launched the model in March, causing losses to investors after disappointing sales.

The automaker has high hopes for the seven-seat MPV, launched on March 1. Li Auto touted the Mega as a local offering that could shake up the luxury MPV market traditionally dominated by the Toyota Alphard and Mercedes V-class.

Alibaba Group (NYSE: BABA)‘s FQ4 announcement portrays a resilient comeback to growth, suggesting the past four years’ challenges barely impacted its dominance in Chinese e-commerce.

However, a closer look beyond the surface of Alibaba Group Holding (9988 HK)’s FQ4 results announcement reveals that little has actually changed in recent months.

Taobao and Tmall face challenges in a tough, stagnant market; AIDC’s growth largely covers for other Alibaba units’ failings, while AliExpress’s expansion cuts into margins.

Alibaba Group (NYSE: BABA) is undervalued by looking at traditional financial metrics.

The political risk associated with investing in Chinese equities, including BABA, is the Elephant in the Room and the point to be discussed.

I believe Chinese stocks are not investable at this point due to the CCP’s anti-globalization stance and its track record of dismantling Deng Xiaoping’s economic reforms.

BABA is a risky asymmetric bet on the direction of economic policies in China. Political risk is nearly impossible to predict, so I recommend avoiding this stock.

We are more bullish on PDD Holdings (NASDAQ: PDD) orPinduoduo’s 1Q24 results on the back of better monetization of domestic e-commerce business and fast and quality growth of TEMU.

We now expect 1Q24 adjusted earnings to almost double yoy to RMB20 billion, much higher than our previous estimate of 50% yoy growth and exceeding consensus by ~30%.

Moreover, we believe earnings growth will be steady throughout 2024 instead of slowing down as we thought. 10x FY24 earnings against 80% yoy growth lead us to see 50%+ upside.

JD.com(NASDAQ: JD) announced a set of in-line results for 1Q24. Sales growth was 7% yoy, in-line with my 1Q24 preview.

Operating profit margin for the core JD retail business declined by 0.5ppt yoy to 4.1%, which is also in-line with my preview.

The positive surprise was a big reduction in losses in the JD logistics business, which brought the overall non-GAAP net profit growth to 17% yoy for 1Q24.

China’s leading online grocer’s return to growth in the first quarter follows an overhaul that saw it withdraw from smaller markets to focus on larger cities

Dingdong (NYSE: DDL)’s revenue grew slightly in the first quarter, ending more than a year of revenue contraction

The company recorded its second quarterly net profit since its listing and said it expects both revenue and profit to post “considerable year-over-year growth” this year

Kuaishou Technology (HKG: 1024 / 81024 / LON: 0A74 / OTCMKTS: KUASF / KSHTY), akin to TikTok in the West, competes with ByteDance’s Douyin (the Chinese TikTok) in China. To clarify and avoid any confusion: Bytedance is the owner of both Douyin and its sister app, TikTok. What distinguishes Kuaishou from other social media platforms, including Bilibili (NASDAQ: BILI) and Xiaohongshu, is its strong presence in lower-tier cities.

Previously, Kuaishou’s user base was considered a weakness. The argument was that brands and advertisers would prefer Douyin due to its higher presence in first-tier cities and more affluent user base.

This is the full analysis – the executive summary I published already last week.

In summary, Kuaishou Technology (HKG: 1024 / 81024 / LON: 0A74 / OTCMKTS: KUASF / KSHTY), with its unique foothold in China’s lower-tier cities, is ideally positioned to benefit from new growth opportunities in these regions. Its user base is becoming increasingly valuable. Currently, at an inflection point after just turning a profit, Kuaishou is poised for greater profitability thanks to operational leverage and various levers they can pull to further increase profitability. Together with their strong balance sheet, they appear to be undervalued at current prices.

GDS Holdings Ltd (NASDAQ: GDS)’ stock has been dragged down by weak growth in China and an overextended balance sheet, but management is on track to achieve positive cash flow and a rebound in share price

GDS Holdings (GDS.O; 9698.HK) (“GDS”) is an owner and operator of data centers in China and Southeast Asia, with a market cap of about USD 1.75 billion (USD 9.50 per ADS as of 17 May 2024 market close). In this brief, we explain how GDS’ share price could improve to above USD 14 if management can improve data center utilization, generate free cash flow and de-leverage debt. Favorable macro tailwinds (e.g. easing of geopolitical tensions, generative AI-driven cloud demand, and recovery of onshore financial markets) could further drive a valuation re-rating.

The online car loan facilitator’s business is growing at a similar pace to China’s auto market, which has decelerated after years of strong growth

Transactions on Yixin Group (HKG: 2858 / FRA: 1YX)’s car loan platform increased about 10% in the first quarter, on par with growth the broader market during the period

Despite China’s better-than-expected GDP growth in the first quarter, Yixin remains challenged by weak domestic consumption

Is Luckin (OTCMKTS: LKNCY) the reason for Starbucks Corp (NASDAQ: SBUX)’s sales decline in China? Is Luckin’s expansion sustainable? What can we learn from this competition?

Both Starbucks and Luckin Coffee recently unveiled their Q1 2024 earnings, eliciting varied market responses.

In China, Starbucks faced a challenging quarter with comparable store sales declining by 11%, attributed to an 8% drop in average ticket sales. Meanwhile, Luckin has stayed committed to rapid expansion, opening over 2,000 stores in Q1, albeit at a slower pace than usual. Who is winning in China’s competitive coffee scene?

Tune in as we delve into the latest results of these two coffee giants, the evolving landscape of coffee consumption in China, and examine the competitive dynamics between traditional giants and agile disruptors in the digital age.

It has a leading market share in the inspect repellent sector in China. The company’s business deteriorated in 2021 and 2022 as the Chinese consumers spent less on the company’s core products such as the insect repellents.

Cheerwin Group Ltd (HKG: 6601 / FRA: 1RQ) is a strong turnaround story with significant earnings growth in 2023 with solid dividend yield. It is the number one player in the inspect repellent sector in China.

Cheerwin’s current price is 79% lower than the IPO price. However, Cheerwin’s shares are up 35% YTD, sharply outperforming Hang Seng index which is up 13.6% YTD.

We found Cheerwin (6601 HK) using Smartkarma’s Smart Score Screener system. We used the following screening methodology: Market cap – More than $300 million Dividends = 5 only.

China’s leading vaping company said its revenue nearly tripled in the first quarter, though the figure remains well below levels from before a 2021 regulatory clampdown

RLX Technology (NYSE: RLX)’s revenue tripled in the first quarter and the company returned to profitability, as it recovers from a regulatory clampdown

The company said its recent international expansion is “progressing well,” as it seeks to diversify beyond its home China market

The disposable diaper maker exports a majority of its products, selling more to Russia than it does in its home China market

Soft International has filed for a Hong Kong IPO, classifying its core line of diaper products as ‘humanitarian’ to skirt Western sanctions on trade with Russia

The company’s sales to Russia accounted for 58% of its revenue in 2023, up from 50% in 2022

[Lifestyle products retailer] MINISO Group Holding (NYSE: MNSO) reported C1Q24 revenue in-line with our estimate/consensus. Non-GAAP NI beat our estimate/consensus by 4.2%/2.6%, mainly due to better gross margin from IP sales.

Company cited pressure on profits in C2Q24 due to store expansion, yet we still believe MNSO can maintain an OPM of 20% for entire 2024

We maintain a BUY rating on the stock and maintain TP at US$34/ADS

With policy support, railway rolling stock is expected to be replaced and upgraded at an accelerating pace, boosting revenue for railway equipment makers

Yancoal Australia (ASX: YAL / HKG: 3668 / FRA: YA1 / OTCMKTS: YACAF) is less likely to do buybacks for now. The company wants to maintain its free float to increase the chances of index inclusion for its Australian shares.

YACAF has a substantial cash position that gives it the financial capacity to engage in inorganic growth investments.

I maintain my Hold rating for Yancoal Australia following an assessment of the company’s capital allocation approach.

Hong Kong-listed Macau Legend Development Ltd (HKG: 1680 / OTCMKTS: MALDF) has completed the planned disposal of its Laos casino resort, announced the company in a filing on Thursday.

The exercise regarding Savan Legend Resorts (pictured in a file photo) in Savannakhet, Laos, had been pushed back for several times since February, according to previous company filings.

Macau Legend might soon also dispose of its other business asset outside of Macau. It was reported over the weekend that the government in the island nation of Cape Verde was in talks with the firm revert the latter’s concession to develop and operate a casino resort in the West African country.

In Macau, the company owns a tourism complex called Macau Fisherman’s Wharf, a waterfront area close to the Outer Harbour Ferry Terminal on Macau peninsula. The venue features a casino called Legend Palace, promoted by Macau Legend under a so-called services agreement with Macau licensee SJM Holdings (HKG: 0880 / FRA: 3MG1 / KRX: 025530 / OTCMKTS: SJMHF / SJMHY).

The premium beer company has struggled to maintain its post-pandemic sales pace in a fiercely competitive market, but major sporting events later this year could boost demand

Budweiser Brewing Company APAC Limited (HKG: 1876 / OTCMKTS: BDWBY / BDWBF)’s first-quarter revenues slipped 0.4% and profits fell 3.4%, sagging from elevated levels a year earlier and dampened by bad weather

Market watchers say earnings may pick up in the second half, stimulated by events such as the Paris Olympics, but rivalry in the premium beer business is heating up

Finally, there are companies that are listed in Hong Kong but don’t have much exposure to China in the first place. Some of them, such as Samsonite International SA (HKG: 1910 / FRA: 1SO / OTCMKTS: SMSOF), Prada SpA (HKG: 1913 / FRA: PRP / PRP0 / OTCMKTS: PRDSY / PRDSF), UC OK Rusal MKPAO (HKG: 0486) and L’Occitane International (HKG: 0973 / FRA: COC / OTCMKTS: LCCTF), are listed in Hong Kong because of the high valuation multiples that the market used to offer. Others, such as Cambodian casino operator NagaCorp (HKG: 3918 / FRA: N9J / OTCMKTS: NGCRF) and Indonesian investment holding company First Pacific (HKG: 0142 / FRA: FPC / OTCMKTS: FPAFY / FPAFF), chose Hong Kong as a home for their businesses.

To name a specific example, our entire group was impressed by what we saw when visiting Plover Bay Technologies (HKG: 1523 / OTCMKTS: PBTDF).

On this particular trip, we visited blue chip companies but also little-known small-caps. One that I found a surprisingly interesting story was the combo of Lion Rock Group Ltd (HKG: 1127)and Left Field Printing Group Ltd (HKG: 1540).

Cafe De Coral (HKG: 0341 / OTCMKTS: CFCGF) is the best-known of Hong Kong’s restaurant chains, with roughly 500 stores in Hong Kong and Mainland China. It sells typical Hong Kong fare, a mix of Chinese and Western cuisine at affordable prices.

CK Hutchison (HKG: 0001 / FRA: 2CKA / OTCMKTS: CKHUY / CKHUF) has been in my portfolio for over 6 years and has delivered disappointing results. The dividend yield has been nice. Apart from the dividend, the only good thing is that I have led the position to decline in relevance in my portfolio. By good performance of other stocks and new money not being invested in CK Hutchison.

The answer is quite simple. I still like the assets and management (my views have not changed much since 2018). While I tend to stick to easier investment theses for newer investments, I have a decent track record with sum-of-the-parts investments (thanks to Berkshire Hathaway, Bollore, and Investor AB).

In the case of CK Hutchison the sum of the parts still looks very attractive.

This is a quick note discussing the buyout offer of L’Occitane International (HKG: 0973 / FRA: COC / OTCMKTS: LCCTF) by it’s majority shareholder Reinold Geiger and Blackstone/Goldman who are advising/backing him in this deal.

The former casino powerhouse’s revenue rose 73% in the first quarter, but it continued to lose money as it lagged many of its peers

SJM Holdings (HKG: 0880 / FRA: 3MG1 / KRX: 025530 / OTCMKTS: SJMHF / SJMHY)lost HK$74 million in the first quarter, narrowing sharply from a year earlier, as Macau’s gambling industry recovered post-pandemic

Investment banks aren’t bullish on the casino operator, with Morgan Stanley maintaining an “underweight” rating on the company

Macau-based casino operator Galaxy Entertainment (HKG: 0027 / OTCMKTS: GXYEF) plans to start rolling out ‘smart’ casino tables at its casinos from July onwards. The news was provided by the firm in a conference call with investment analysts following it announcing its first-quarter results on Tuesday.

“Smart tables [are] to be launched from July onwards”, wrote brokerage Jefferies Hong Kong Ltd, in a note citing the key points discussed by Galaxy Entertainment’s management during the analyst briefing.

The first thing that jumps out is that Macau E&M Holding Ltd (HKG: 1408) is a very small company. The market cap is currently $72.1m Macau Pataca (MOP), or around $9m USD. The free float is much smaller than that because the company’s insiders own 75% of the outstanding shares. So the free float is probably only around $2.3m USD. This company is really among the smallest of Hong Kong listed companies. Usually these very small companies have terrible issues. I think Macau E&M looks a lot better than most in that group though.

Macau E&M is an electrical and mechanical (“E&M”) engineering services works contractor in Macau. They provide HVAC system works and low voltage system works for the public sector and the private sector. Their private sector customers are primarily hotels and entertainment resorts. Demand from this group is tied to the performance of the casino’s in Macau.

Silicon Motion Technology Corp (NASDAQ: SIMO) reported its first quarter of FY2024 results earlier this month, confirming what I believe is more upside for the stock in 2024.

I expect this upside will be driven by Silicon Motion’s position as a global supplier of NAND flash controllers during a moment where pricing and unit demand should recover.

The company raised its FY2024 revenue outlook to $800 million to $830 million for a 25-30% year-over-year growth rate, versus the earlier guidance for 20-25% growth.

I share my thoughts on Silicon Motion stock here and why I think it has more upside in 2024.

Taiwan Printed Circuit Board Techvest Co. Ltd. (TPE: 8213) is the world’s largest LCD printed circuit board(PCB) manufacturer. Printed circuit board is a USD 80B sector with a CAGR of 3.82% that is an integral part of the electronics industry. The company has been profitable for 21 consecutive years and paying dividends 20 years straight. Trading is available on Interactive Brokers and English filings are available.

With an EV/EBT under four, there is tremendous value here. It has a robust history of profitability and treating the shareholders fair. Liquidity is healthy too. A portfolio of such companies should provide good performance over time.

We would avoid participating in this block deal sale and we have a Negative view of HD Hyundai Heavy Industries (329180 KS) over the next one year. Three major reasons why we are negative are as follows:

According to Maekyung Business Daily, SK Innovation (KRX: 096770) maybe planning to sell its controlling interest in SK IE Technology (KRX: 361610) which produces separators for rechargeable batteries.

SK On is experiencing financial difficulties due to the sluggish demand for EVs. SK Innovation’s 61.2% stake in SK IET is worth 2.5 trillion won.

SK IE Technology had an earnings shock in 1Q 2024. It had sales of 46.2 billion won (67.8% lower than consensus) and operating loss of 67.4 billion won 1Q 2024.

On 16 May, it was reported that the Korean financial regulators have approved DGB Daegu Bank to become the 7th commercial bank in Korea.

DGB Daegu Bank is the core entity of DGB Financial Group (KRX: 139130) which currently has a market cap of 1.4 trillion won (US$1.0 billion).

This change will allow the company to expand in the more lucrative metropolitan Seoul and other regions in Korea. We have a positive view of DGB Financial Group (139130 KS).

DGB Financial’s dividend yield averaged 6.8% from FY 2019 to FY 2023.

Paradise Co Ltd (KOSDAQ: 034230), an operator in South Korea of foreigner-only casinos, is one of seven companies added to a list of firms subject to enhanced supervision by the country’s antitrust regulator, the Fair Trade Commission.

The information was reported by South Korea’s Yonhap News Agency, saying the newcomers boosted the list to 88 companies.

One of three sons of NagaCorp (HKG: 3918 / FRA: N9J / OTCMKTS: NGCRF)’s late founder Chen Lip Keong, appointed to a chief executive role there in April 2022, has had his employment terminated at the casino group with effect from Thursday, the firm said in a filing to the Hong Kong Stock Exchange after trading hours that day.

According to the filing, the departure of Chen Cherchi from the role of CEO – finance and treasury involved “possible disagreement” between the outgoing executive and the firm over his contract termination.

The departing executive’s father, Chen Lip Keong, died in December last year. Prior to his death, a succession plan saw three sons appointed to joint CEO roles at NagaCorp.

The tender offer price in this second tender offer is 8,750 won (same as the first tender offer). The second tender offer will last from 16 May to 5 June.

In the first tender offer, only about half of the target was reached. There was a strong backlash from investors due to low tender offer price.

Ecopro Materials’ share price is likely to face continued weakness, especially with the potential for a major block deal sale by BRV Capital and end of the lock up period.

We believe that HD Hyundai Marine Solution’s share price has surged above its intrinsic value. More insiders are likely to start selling HD Hyundai Marine Solution in the coming months.

Our base case valuation of Innospace is target price of 51,481 won per share (12 month view), which is 28% higher than the midpoint of the IPO valuation range.

We estimate Innospace to generate sales of 1.8 billion won in 2024, 28.7 billion won in 2025, and 58.3 billion won in 2026.

Innospace is involved in the satellite launch vehicle production and launch service business.

GoTo Gojek Tokopedia (IDX: GOTO / FRA: CK8 / OTCMKTS: GTOFF) booked an encouraging set of 1Q2024 results which provided a first look at the new structure, whereby suddenly e-commerce became cashflow positive for the company.

The company booked strong headline growth with core GMV increasing by +32% YoY, despite incentive & product spending decreasing by -31% YoY, whilst adjusted EBITDA losses fell -89% YoY.

GoTo will drive growth less through incentives and more through innovative products, increasing the user base, and focusing on retention through its subscription products, with fintech becoming increasingly important.

Encouraged by all the absurdly-cheap stocks in HK, I decided to do an A-Z screening on Singapore stocks. Haw Par (SGX: H02 / OTCMKTS: HAWPF) came out as my local favorite.

The Tiger Balm brand may account for about SG$ 3-4 per share (or more) in value.

For the Tiger Balm brand alone, I would be tempted to buy some shares. However, most of the value in Haw Par seems to be represented by other cash and financial assets, predominantly the stake in United Overseas Bank (SGX: U11 / FRA: UOB / UOB0 / OTCMKTS: UOVEY / UOVEF).

Business intelligence (>90% mix); Organizing business awards and conducting business impact assessments on these awards. Awards include SME100, HR Asia Best Companies to Work for in Asia, CXP Best Customer Experience Awards and the Golden Bull Award.

Description; $TCU provides credit and risk information solutions across Singapore, Malaysia, Cambodia and Myanmar, mostly through joint ventures with Dun & Bradstreet and Equifax. It is the dominant market leader in Singapore, Cambodia and Myanmar with data for Financial Institutions.

Personally, I do wonder about brand strength within the Delfi chocolate brands portfolio. I would certainly expect higher (normalized) profit margins from a chocolate brand owner.

Description; $BHU operates luxury yacht marinas under the ONE15 Marina brand, and a yacht chartering business with a fleet of more than 50 luxury yachts, under ONE15 Luxury Yachting.

ThaiBev is the dominant spirits company in Thailand, with bigger ambitions in the broader region. Besides beer and spirits, there are some other (smaller) staples activities in the mix too.

The bank has offered to purchase the remaining shares of Great Eastern Holdings (SGX: G07 / OTCMKTS: GEHDY), or GEH, that it does not already own in a voluntary unconditional general offer.

This move came right after the lender announced a sparkling set of earnings for the first quarter of 2024 (1Q 2024) as higher interest rates buoyed its total income.

Will OCBC’s move benefit the bank’s earnings and help it to achieve better results? Let’s dig deeper to find out.

We feature four Singapore industrial REITs that sport distribution yields of 6.6% or higher.

AIMS APAC REIT (SGX: O5RU / OTCMKTS: ACIRF), or AAREIT, owns a diversified portfolio of 28 industrial properties in Singapore (25) and Australia (3).

Mapletree Logistics Trust (SGX: M44U / OTCMKTS: MAPGF), or MLT, is a logistics REIT with a portfolio of 187 properties spread across eight countries.

ESR-Logos REIT (SGX: J91U / OTCMKTS: CGIUF), or ELR, is an industrial REIT with a portfolio of 72 properties in Singapore (52), Australia (19) and Japan (1).

Frasers Logistics & Commercial Trust (SGX: BUOU / OTCMKTS: FRLOF), or FLCT, is an industrial and commercial REIT with a portfolio of 112 properties worth approximately S$6.8 billion.

The head of Genting Singapore (SGX: G13 / FRA: 36T / OTCMKTS: GIGNF / GIGNY) says the company would have interest in collaborating in an integrated resort (IR) project with casino in the United Arab Emirates (UAE), if such opportunity presented itself.

Genting Singapore’s management said the group’s focus was now on the expansion project of Resorts World Sentosa. The company has pledged to invest SGD6.80 billion (US$5.05 billion) to upgrade and expand the complex, a project known as RWS 2.0.

“Extremely high” hold in the VIP gambling segment at Resorts World Sentosa (pictured) helped Genting Singapore (SGX: G13 / FRA: 36T / OTCMKTS: GIGNF / GIGNY)’s business performance in the first quarter, but the issue of player bad debt and other business costs still lurk in the background for the current year, say several brokerages.

Genting Singapore – operator of one half of Singapore’s casino duopoly – saw quarterly net profit circa double quarter-on-quarter and year-on-year when it reported first-quarter trading highlights in a Friday after-hours filing to the Singapore Exchange.

Yesterday (14 May) evening Asia time, Shopee’s parent Sea Limited (NYSE: SE) released its Q1 2024 results. It is a good set of results: digital entertainment is back to growth with its star game Free Fire recovering, Shopee increased its GMV and take rate while reducing sales & marketing expenses significantly.

The market reacted mildly positively to the results, sending Sea’s share price up by 2.79% at the end of the first trading day after the release. There were some swings during the intraday trading but much less compared to the day after the previous earnings report. The share price had actually gone up by almost a quarter in the month leading up to the current release of earnings.

Sea Limited (NYSE: SE), the Singapore-based e-commerce conglomerate, saw its stock rise nearly 15% after reporting strong results across all three major businesses.

The gaming division saw a sharp resurgence in paid users, the result of new releases within existing games and the continued popularity of Free Fire.

E-commerce revenue also grew more than 30% y/y, while improvements in logistics helped improve profitability on a sequential basis.

The company is also seeing soaring profitability in its digital financial services arm, as its loan loss ratios improve year over year.

With that out of the way I want to introduce you all to Centurion Corporation Ltd (SGX: OU8), a Singapore based worker and student housing provider. Their student housing services are based out of mainly the UK, with some exposure to Australia and the US and accounts for around a quarter of their revenue. Meanwhile their worker accommodation operations are based mainly in Singapore with some Malaysian exposure and accounts for the other 3 quarters of revenue. The company operates in an interesting niche that is experiencing a large amount of growth, with demand for student housing and worker accommodation surging in the years since the pandemic.

The company has a pretty impressive track record for a cheap, emerging market small cap.

GHCL Textiles Ltd (NSE: GHCLTEXTIL / BOM: 543918)Aiming 25-30% revenue growth along with 15-20% average marginssignificantly increase the profitability of the company.

Entering into value-added products like Functional fabrics and setting up their own manufacturing plant for fabric.

Management Guidance on yarn prices, capex and debt profile of the company.

Zen Technologies (NSE: ZENTEC / BOM: 533339) expands product range to drones, anti-drone systems, and medical simulators, enhancing opportunities beyond government contracts.

Strong order book of Rs 1,401 crore, significant R&D investment, and government support for indigenous defence manufacturing drive growth.

Zen Technologies (ZEN IN) diversified product portfolio and strategic government support position it well for significant growth in the defence and simulation markets.

KASPI (LON: 80TE / FRA: KKS) is Kazakhstan’s most valuable listed company, offering a super app with features like payments, e-commerce, travel, and government services.

The company has a dominant market position and is growing rapidly, with a low valuation and a policy of returning capital to shareholders.

Kaspi.kz’s revenue and net income quality is improving due to marketplace and payments growth. Kaspi is also expanding internationally.

We rate the stock a BUY with a conservative target price of $129.

The war in the Middle East presents both opportunities and drawbacks for Elbit Systems Ltd. (NASDAQ: ESLT), with increased demand but also labor and logistics pressures.

Elbit Systems has shown strong growth in backlog and adjusted operating income, but operating margins have weakened.

Near-term demand and labor costs driven by the war are important factors to watch, but the company can rely on long-term global demand trends.

Checkers Sixty60 has upped its e-commerce game as it announces that it’s beta testing the new and improved version of its app, enabling customers to shop for more than 10 000 larger Hyper products, with same-day delivery scheduled within a 60-minute time slot.

The move comes hot on the heels of Amazon’s launch in South Africa more than a week ago.

However, Shoprite Group(JSE: SHP) and its offerings, including Checkers Sixty60, is a very successful and trusted brand in South Africa and is no pushover.

Checkers Sixty60 is currently the number one grocery app in South Africa, with more than 4.5 million downloads. It is available at 505 locations and its sales have increased over tenfold since the first half of 2021.

Nampak Ltd (JSE: NPK / FRA: NNZ0), Africa’s biggest packaging group that is struggling through a severe restructuring due to high debt, saw its share price surge yesterday after it announced the $68.5 million (R1.25 billion) sale of its Nigerian business.

Proceeds from the disposal would go towards reducing Nampak’s debt. The book value of the assets being sold, at September 30, 2023, was R69.4m.

South Africa’s coal and platinum group metals (PGM) sectors will likely remain muted in terms of productivity and earnings for the remainder of this year, analysts at BMI Research said yesterday, citing the persistent challenges afflicting the industry and dim prospects for a quicker turnaround post the May 29 elections.

“The South African mining industry is to face further contraction in 2024 as persistent challenges linked to power supply disruptions, rail and port bottlenecks and the weak outlook for coal prices weigh on the sector.”

Lower mining production and a plunge in mineral sales in the first quarter of this year is dragging down South Africa’s gross domestic product (GDP) growth, and is reflecting reduced profitability in the sector despite a rally in the price of gold.

Data released by Statistics SA (Stats SA) yesterday showed mining production in South Africa declining by 1.7% on a quarter-on-quarter and year-on-year basis in the first quarter of 2024 compared with the fourth quarter of 2023, dragged down by platinum group metals (PGMs), coal and surprisingly gold, whose output volumes lowered by 2.9%.

Anglo-American (LON: AAL / JSE: AGL / OTCMKTS: NGLOY) said that following its February announcement that it was reconfiguring Amplats[Anglo American Platinum (JSE: AMS / FRA: RPHA / FRA: RPH1 / OTCMKTS: AGPPF / ANGPY)], it would be separating from the company in which it holds a 79% stake, adding that its portfolio and structure were simpler without Amplats.

Seleho Tsatsi, a mining analyst at Anchor Capital, yesterday said that spinning off Amplats was being considered before the BHP Group (NYSE: BHP) bid, although the offer could well have sped up the decision.

Miners in South Africa, where the world’s largest platinum reserves are held, have been battling.

Impala Platinum Holdings (JSE: IMP / LON: 0S2J / FRA: IPHB / OTCMKTS: IMPUY / IMPUF) could well shut some shafts after half-year profits for the period to the end of December 2023, slumped to R1.7bn compared to R14.8bn a year earlier.

Platinum and Palladium have both rallied well off their lows. Miners have strong balance sheets and are in a position to capitalize on stronger metal prices, while South Africa – the main country providing supply to the market – looks to be stabilizing politically.

Of these equities, South Africa focused Anglo-American (LON: AAL / JSE: AGL / OTCMKTS: NGLOY) is the largest by far, with Impala Platinum Holdings (JSE: IMP / LON: 0S2J / FRA: IPHB / OTCMKTS: IMPUY / IMPUF) and Sibanye Stillwater Ltd (NYSE: SBSW) very close to each other in the second and third positions. Sibanye is also interestingly exposed to a number of other metals, including gold, which has been on a tear recently.

From a balance sheet perspective, we can see that Sibanye and Anglo American are the most levered in the sector. In my view, none of the names are unreasonably levered, and remember – leverage and upside come together.

If South Africa really goes to hell after the election (and it’s hard to imagine much more of a descent, outside of outright cannibalism), you’ll really want to own the physical metals above all. But if I did own a stock, I’d want something with an upside call option outside of South Africa, or stick with a very conservative name.

The U.S. and China are competing to acquire the metal essential for EVs and data centers. It is also at the center of a $43 billion takeover battle.

While London-listed Anglo produces a range of commodities, from diamonds to nickel, Australia’s BHP has made clear that it most prizes the company’s copper assets.

BHP Group (NYSE: BHP) is likely to make another revised and firm offer for Anglo American after the London and Johannesburg-listed resource firm yesterday announced a strategy to spin-off De Beers and Anglo American Platinum (Amplats) [Anglo American Platinum (JSE: AMS / FRA: RPHA / FRA: RPH1 / OTCMKTS: AGPPF / ANGPY)], but retaining Kumba Iron Ore (JSE: KIO / OTCMKTS: KIROY / KUMBF), ahead of the 22 May deadline stipulated by London listing rules.

Business groups slammed the signing of the bill into law, saying in its current form the NHI Bill was fundamentally flawed, would damage the economy and dent confidence in investing in South Africa.

South African business duo Eldrid Jordaan and Goitse Konopi listed their new technology venture, Suppple, on the Luxembourg Stock Exchange on Tuesday.

The market cap is £200 million (R4.6 billion) and the share price £2. The listing enhances Suppple’s financial stability and investment attractiveness, facilitating expansion into new markets and sectors.

Suppple is an infrastructure-as-a-service) API technology platform designed to assist governments of all sizes, across the globe, to rapidly organise, digitise and automate their functions.

Suppple’s Business Process Outsourcing (BPO) through Resolv Global, call centre and collection agents, also enhances BPO services in South Africa, Kenya and Columbia with customised call centre solutions. By integrating chatbots and AI technology, Suppple improves customer and employee experiences, optimising operational efficiency and effectiveness, thus yielding service quality.

MercadoLibre (NASDAQ: MELI) recently reported its earnings for Q1 of 2024.

The company has continued its robust trend, with Brazil and Mexico being their primary growth engines.

Both markets recorded growth in Gross Merchandise Value (GMV) of approximately 30% YoY. This expansion was propelled by their strategic investments in tech infrastructure, targeted marketing campaigns, and focus on enhancing user experience.

“In our view, the exit of Prates is a deterioration of Petrobras(NYSE: PBR / PBR-A)governance and a downside risk for the investment thesis,” Citi analysts Gabriel Barra and Andres Cardona told clients in a note. “The new CEO arrives with the pressure to fulfill the investment plan and accelerate the capex expansion, which may negatively impact the company’s dividend payment.”

Despite her close ties to the government, Chambriard faces significant challenges in balancing the interests of private shareholders, government directives, and consumer sensitivities to fuel price changes. Refinery expansions in the region are notoriously prone to delays and cost overruns, complicating the push for swift investment execution.

Chambriard’s agenda includes navigating Petrobras’s role in petrochemical producer Braskem (NYSE: BAK), where the company is the second-largest shareholder. The potential acquisition of Novonor’s stake in Braskem remains a contentious issue, with Lula advocating for Petrobras to strengthen its petrochemical operations.

Petrobras(NYSE: PBR / PBR-A)‘ Q1 earnings missed estimates, causing a selloff, but I believe it is just noise as the company’s profitability remains unparalleled, allowing to deleverage and keep shareholders happy.

PBR is increasing CAPEX to build long-term value for shareholders and has improved its financial position.

The company dominates Brazil’s oil and gas sector and is poised for robust oil production in the coming years. The valuation is attractive with significant upside potential.

Investors face substantial political risks, underscored by the information that the CEO was fired by Brazil’s president, but the upside potential outweighs all the risks.

Petrobras(NYSE: PBR / PBR-A) released results 5.5% below consensus. But what caught the attention was the fired CEO, which shows increasing risks to corporate governance.

However, the company reported another quarter with good cash generation and healthy leverage. Additionally, its valuation continues to be discounted compared to its peers.

The new CEO is expected to increase investments in refinery reforms, the naval industry and exploration. And except for exploration, other investments have not brought good returns in the past.

Petrobras(NYSE: PBR / PBR-A)‘s dividend payouts and yields remain rich despite the recent volatility, making it a compelling buy for dividend-oriented investors.

The company has reported mixed earnings for FQ1’24, with the planned maintenance, lower production volume, higher operating expenses, and forex impact contributing to the weaker results.

Despite so, its spread remains rich, attributed to the low break even point and elevated Brent spot prices compared to pre-pandemic averages.

At the same time, PBR’s discounted valuations are mostly due to geopolitical headwinds, with its strategic investment plan potentially leading to upside potentials in the future.

It goes without saying that its rich dividend investment thesis is only suitable for those with higher risk appetite, attributed to the volatile geopolitical developments.

BRF Brasil Foods SA (NYSE: BRFS / BVMF: BRFS3) is a Brazilian meatpacker specializing in poultry, pork, and processed foods. The company operates globally and owns Brazil’s leading meat-based product brands, Sadia, Perdigao, and Qualy.

4Q23 and 1Q24 earnings sent BRF’s stock up 30%, thanks to a cyclical recomposition of margins. The company’s EBITDA margins went from 5% one year ago to 16% in 1Q24.

The margin recomposition was expected in a cyclical industry with volatile supply (live animals and feed) and demand (processed meat) markets.

A reversion of margins could also occur in future periods. That is why I prefer a cycle-average approach to valuation. Considering that approach, the stock is still expensive, so I maintain my Hold rating.

With revenue, ROE, and NIM continuing to expand at elevated levels, the growth story remains intact.

With this earnings release the stock’s PE should decrease by approximately $7.81 based on the new diluted EPS and post-market trading price, improving the valuation.

Although not everything in this release was all sunshine and rainbows, Q1 appeared strong, I am reiterating my high conviction in the stock and going with a strong buy rating.

Brazilian FinTech StoneCo Ltd (NASDAQ: STNE)‘s stock dropped 10% after reporting lower-than-expected revenue and EBIT, but the company remains on track to exceed its guidance for the year.

StoneCo’s customer base growth rate is slowing down, with only 200k new customers registering last quarter.

Costs have gone up because of one-off marketing expenses.

StoneCo’s credit division is performing exceptionally well. Increasing borrowers and volume will drive future profits. Even more so when the loan loss provision rate will be adjusted downwards.

At the current price, you get this credit division for free.

Lithium-ion batteries are likely to be most affected by a new round of U.S. tariff hikes designed to prevent the American market from being flooded with cheap Chinese goods.

On Tuesday, the Biden administration announced it would increase tariffs on $18 billion worth of Chinese imports across strategic sectors including electric vehicles (EVs), lithium-ion batteries, semiconductors and medical devices, in a move it described as a “response to China’s unfair trade practices” that “are threatening American businesses and workers.”

The Biden Administration on Tuesday announced a decision to increase tariffs on $18 billion worth of Chinese imports across strategic sectors including electric vehicles (EVs), semiconductors, lithium-ion batteries and steel.

The move is part of a broader strategy said to prevent Chinese manufacturers from undercutting their U.S. counterparts and threatening American jobs.

Freight rates for Chinese container exports spiked over the past two weeks, driven by increased demand overseas and the intensifying crisis in the Red Sea, with Yemen’s Houthis announcing last week they attacked three more ships.

The Shanghai Containerized Freight Index, which reflects changes in spot freight rates from the port city to export destinations such as Europe, reached 2,305.79 on Friday, up nearly 19% from end of April and the highest since late September 2022, data from the Shanghai Shipping Exchange showed.

The Hong Kong Stock Exchange’s decision to stop disclosing certain real-time data for northbound trading under the Stock Connect program will make the market less transparent but more stable, market insiders said.

Real-time figures for sales, purchases and total turnover through the northbound link, which allows overseas investors to trade Chinese mainland-listed stocks through Hong Kong, have been unavailable since Monday, according to acircular issued by the Hong Kong exchange.

The number of unemployed persons increased by 330 000 to 8.2 million, up from 7.9m in the previous quarter, marking the highest figure since comparable records began in 2008.

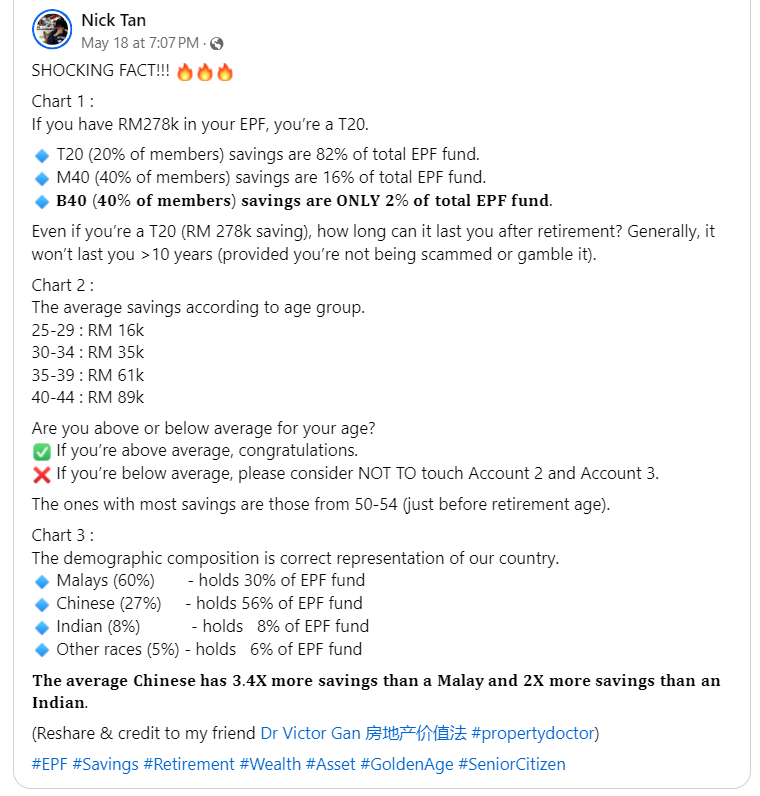

🇲🇾 Note: This showed up in my Facebook feed as someone shared it – I thought it was interesting as the average Malaysian probably has more saved up in their EPF account than your average American has in their savings + retirement accounts:

The People’s Republic of China (PRC) is the principal strategic competitor of the United States. In addition to antagonism in other domains, this rivalry entails escalating technological competition. No country is technologically self-sufficient, but the United States’ reliance on China’s considerable market share in the critical minerals industry for semiconductor supply chains creates a dependency that turns a trade imbalance into a potential national security threat. Chips are ubiquitous in all modern technology, and their relevance and worth will only expand in the coming years. The countries that are able to secure their own supply chains for critical technologies will be in a position to write the rules of global economic governance for years to come.

Note: Investing.com has a full calendar for most global stock exchanges BUT you may need an Investing.com account, then hit “Filter,” and select the countries you wish to see company earnings from. Otherwise, purple (below) are upcoming earnings for US listed international stocks (Finviz.com):

Frontier and emerging market highlights from IPOScoop.com and Investing.com (NOTE: For the latter, you need to go to Filter and “Select All” countries to see IPOs on non-USA exchanges):

🏁 Emerging Market ETF Launches

Climate change and ESG are some recent flavours of the month for most new ETFs. Nevertheless, here are some new frontier and emerging market focused ETFs:

I have changed the front page of www.emergingmarketskeptic.com to mainly consist of links to other emerging market newspapers, investment firms, newsletters, blogs, podcasts and other helpful emerging market investing resources. The top menu includes links to other resources as well as a link to a general EM investing tips / advice feed e.g. links to specific and useful articles for EM investors.

Disclaimer. The information and views contained on this website and newsletter is provided for informational purposes only and does not constitute investment advice and/or a recommendation. Your use of any content is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the content. Seek a duly licensed professional for any investment advice. I may have positions in the investments covered. This is not a recommendation to buy or sell any investment mentioned.

No. of Members (Million) B40 Savings (RM Billion) M40 6.43 Average Savings (RM) T20 11.01 6.43 Median Savings (RM) Total 3.21 1,713 180.23 16.07 1,063 896.70 28,032 20,660 1,087.94 278,941 67,686 170,266 10,898'")

Below 25 Savings (RM Billion) 1.92 25-29 30-34 35-39 Average Savings (RM) 2.24 10.91 Median Savings (RM) 2.12 36.95 40-44 5,674 2.03 74.95 1.82 16,505 35,390 125.04 45-49 50-54 55-59 3,372 9,642 1.63 161.95 1.45 60-64 198.24 15,572 24,711 30,658 1.14 200.60 65 and above 0.65 Total 61,606 89,226 121,287 121 137,903 107,922 118,779 118 122.84 40,673 1.07 76.74 38,731 16.07 79.72 11,115 8,122 1,087.94 74,157 67,686 2,400 10,898'")

No. of Members (Million) Bumiputera Savings (RM Billion) Average Savings (RM) 9.76 Malay Other Bumiputera Median Savings All Age (RM) 371.24 8.13 Chinese Median Savings Age Below 55 (RM) 38,039 332.00 1.63 Indian 7,320 40,827 39.24 4.37 Other Races 7,838 24,110 613.68 1.33 Total 8,254 8,950 5,183 140,285 89.67 0.61 43,595 67,602 5,889 13.36 16.07 14,488 21,795 1,087.94 48,627 1,996 67,686 17,375 10,898 2,181 12,053'")