This is the first post summarizing fund stock, sector, and/or country commentaries by various actively managed emerging market-focused funds from around the world. The original explanation or logic behind these posts has been removed, updated, and placed here: DISCLAIMER: EM Fund Stock Picks & Country Commentaries Posts (and is subject to further updates).

Since this is the first post and follows the end of the year holidays, it mostly covers November EM fund updates that became publicly available in December. Although November was over a month ago, there are over 90+ EM fund stock picks or mentions linked to their Investor Relations or corporate websites for you to further research on your own.

Stock picks range from “new economy” stocks (such as a Chinese autonomous driving technology stock and a super-app stock from Central Asia) to plenty of interesting “old economy” picks in more “mundane” industries or sectors.

Subscribe Now Via Substack

Disclaimer. The information and views contained on this website and newsletter is provided for informational purposes only and does not constitute investment advice and/or a recommendation. Your use of any content is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the content. Seek a duly licensed professional for any investment advice. I may have positions in the investments covered. This is not a recommendation to buy or sell any investment mentioned.

For a further disclaimer and an explanation of the reasoning behind these posts: DISCLAIMER: EM Fund Stock Picks & Country Commentaries Posts.

Note: Where possible, company links are to their respective investor relations or corporate pages. Region and country links are to our ADR or ETF pages where there are further country specific resources (e.g. links to local stock market and media websites). Please report any bad links in the comments section.

[All pay-walled posts have tickers for major stock exchanges (NOTE: Some OTC tickers will be left off IF they see little trading activity) linked to sites such as Finvix, Google Finance (set to open as a 1 year chart), or where ever else stock quotes can be found. Posts starting in March 2023 contain as many 1-year charts (for the main ticker) as possible.]

East Asia

China

For November, the Fidelity China Special Situations PLC (LON: FCSS) noted the peak of new regulatory reforms, especially those impacting Internet stocks, was now in the past. Beijing has already laid out a framework around issues such as anti-monopoly, data protection, data sharing, and cross-selling within an online ecosystem.

Valuations in impacted sectors had moved to historical lows and looked compelling versus their global peers. Stocks in sectors impacted by regulatory changes and geopolitical tensions that declined in November included global pharmaceutical, biopharmaceutical, and medical device stock WuXi AppTec and enterprise and marketing cloud platform stock iClick Interactive Asia. On the other hand, autonomous driving technology stock Pony.ai had advanced.

Meanwhile, Henderson Far East Income Limited (LON: HFEL) noted for November that consumer exposed firms, such as eCommerce stock JD.com and sportswear and sports equipment stock Li Ning, were particularly strong on positive sentiment. On the other hand, the performance of telecommunications and other defensive sectors made way for sectors perceived to benefit from China’s re-opening.

The China Fund, Inc (NYSE: CHN) November update noted that Pinduoduo (one of China’s largest ecommerce platforms that started its businesses with a focus on lower-tier city, price sensitive consumers directly through its interactive shopping experience) had a good performance. CHN pointed out that more Chinese internet platform companies have begun to adapt to new regulations and are trying to set a path to profitability. More encouraging signs of monetization efforts coupled with attractive valuations can potentially help these stocks recover.

On the other hand, the update noted that Baosight (an IT company servicing the digital needs of steel companies and other industrial companies) and Wuxi Lead (a battery equipment manufacturer selling products to battery makers such as CATL) were poor performers. However, these stocks continue to be in secularly growing areas and should benefit from improving sentiment in the A-shares.

The update noted that A-shares stocks had not recovered as quickly given that it takes time to relax COVID measures. Domestic investor sentiment also remained weak.

The Scottish Oriental Smaller Companies Trust plc (LON: SST) November update noted clinical diagnostics stock Autobio Diagnostics had declined as Chinese cities began to reduce COVID testing requirements.

The Utilico Emerging Markets Trust plc (LON: UEM) November update noted that China Gas Holdings was a good performer and was helped by improved market sentiment. The stock showed resilient growth with retail volumes, up 8.0% in the six months to 30 September 2022 and Dollar margins recovering having been impacted by high LNG prices. In addition, it was mentioned that Hong Kong listed integrated energy stock Kunlun Energy (a China National Petroleum Corporation subsidiary) also had a strong rebound from recent lows.

Korea

For November, The Korea Fund, Inc (NYSE: KF) noted the Korean utilities and materials sectors outperformed while the energy sector underperformed on weaker oil prices.

The utilities sector was led by KEPCO, as the Korean government moved to address large losses from rising energy costs. The materials sector was led by traditional chemical companies, as the China reopening news helped turn around the multi-year-low chemicals spreads. Cosmetics companies, such as AmorePacific and LGHH, also outperformed for the same reasons.

The fund noted that after being oversold earlier in the year, mobile payment and digital wallet service KakaoPay and other growth stocks outperformed. As a bet on the EV sector, the fund noted that LG Chemical was much more attractively valued versus its main competitor, LG Energy Solution. Video game developer and publisher NCSoft also met Q3 expectations.

On the other hand, car parts stock Hyundai Mobis along with the auto sector underperformed. Dynamic random-access memory (DRAM) chips and flash memory chip maker SK Hynix also fell after a drop in exports (especially to China). KF noted that China accounts for approximately 40% of Korea’s semiconductor exports and near term exports are expected to remain weak due to worsening demand for semiconductors.

Taiwan

For November, The Taiwan Fund, Inc (NYSE: TWN) noted that Semiconductor and IP companies rebounded sharply after a long correction period commencing in mid-September.

Good market performers for the month included Taiwan Semiconductor Manufacturing Co Ltd., fabless ASIC design service stock Global Unichip Corp, and logic-based non-volatile memory (Logic NVM) R&D stock eMemory Technology Inc.

Poor performers included E Ink Holding Inc (an electronic paper, electronic ink, electronic inkfilm, and other product stock that provides internet of things application services), mobile communications provider Far Eastone Telecom Co., and Genius Electronic Optical Co (however, the update noted expectations of new product spec upgrades in the future for the latter). Dynamic random-access memory (DRAM) chip stock Nanya Technology Corp had high inventory levels.

The update also noted that battery solution provider AES-KY can capture growing demand from data centers and that data centers and cloud servers present long-term growth opportunities.

Meanwhile, SST had noted a good November performance by Parade Technologies (which develops semiconductors for display panels, computers and other consumer electronics), on signs of stabilising demand from end customers and expectations of a recovery in Q1 2023.

SE Asia

Indonesia

The JPMorgan Global Emerging Markets Income Trust plc (LON: JEMI) November commentary noted that Indonesia had been a positive hunting ground for stocks in 2022 – although Bank Rakyat had a weak November performance. However, they had a:

…positive meeting with management, which reinforced the view that the bank is still well positioned in microfinance in Indonesia and can grow profitably over the long term.

However, the BlackRock Frontiers Investment Trust plc (LON: BRFI) November update noted the fundopted to shift fromretail banks to corporate, swapping Bank Rakyat for Bank Central Asia. They also see better potential for margin expansion at Bank Mandiri.

On the other hand, BRFI mentioned conglomerate Astra International (Southeast Asia’s largest independent automotive group controlled by Hong Kong’s Jardine Matheson) had performed poorly. However, the underlying fundamentals of Astra’s vehicle and financing business remained strong despite concerns around pressure on consumer from higher fuel prices and expiring government tax schemes. I suggest reading Joe Studwell’s Asian Godfathers and How Asia Works as Jardine controlled Astra and the auto industry are talked about extensively in both books.

Finally, SST’s November update noted that retail conglomerate Mitra Adiperkasa had risen after reporting better than expected earnings and improving sales growth. The company was expected to benefit from increased spending over the holiday season and into 2023. This would be underpinned by resilient middle- and upper-class consumers.

Malaysia

Malaysia had elections on November 19th which saw long time opposition leader Anwar Ibrahim form a government.

For November, the Singapore registered Pangolin Asia Fund noted that investors should not expect much buying from overseas investors. They suggested watching whether the locals resume buying properties in KL again and start encouraging their offspring to return from overseas after completing their degrees. If that starts to happen, it will signal a change in domestic confidence and lead to more local stock market investing. Then the foreign capital flows will follow.

Finally, the BRFI November update briefly noted that Malaysian banks have likely seen the peak macro environment while post general election economic policy may be constrained by the broad-based coalition government. The update also mentioned Frontken Malaysia (a tech firm that supports the semi-conductor value chain) had rebounded in line with the recovery in share prices of global semiconductor companies.

Thailand

BRFI briefly mentioned Thai mobile phone operator Advance Information Systems which had underperformed on regulatory concerns in the sector.

Vietnam

The December update for the Cayman Islands domiciled AFC Vietnam Fund noted that on November 16th, the VN Index hit a yearly low and had lost 50.4% in USD terms since the beginning of the year. This was despite healthy 2022 earnings growth of Vietnamese companies of around 17% along with a 2022 GDP growth forecast of around 8% and around 6% for 2023.

The massive correction in the Vietnamese stock market was mainly due to disciplinary actions of the Vietnamese government. This included the arrest of high level stock and real estate manipulators and stopping real estate developers who were financing their business expansion by illegally issuing corporate bonds and selling them to local retail investors. They also noted forced selling due to margin calls.

Their December update noted that the VN-Index appears to have reached its bottom mid-November and that the stock market had started to recover strongly.

The November update for VinaCapital Vietnam Opportunity Fund (LON: VOF) noted foreign net buying reached USD682 million in November, the second highest monthly net buying by foreigners in history.

They noted the sharp decline in the stock market at the start of the month was partially triggered by concerns surrounding several large real estate developers, including Novaland and Phat Dat Real Estate, as investors worried about their ability to refinance maturing bonds and the overall lack of access to credit to the sector. Margin call pressure further hurt share prices.

However, Vinhomes (the largest real estate developer in the country) and Khang Dien House (leading landed property developer in southern Vietnam) bucked these trends as their share prices rose.

Lending conditions remain tight in general for real estate developers as banks are naturally reluctant to extend more credit to them. Nevertheless, VOF commented that it could be argued the liquidity crunch is very much a real estate developer problem, rather than a systemwide issue.

It was also noted that Asia Commercial Bank does not do much real estate developer lending (only 1% of its loan book), and most of the loan book is to retail borrowers (at 63% of loans) and SMEs (at 31% of loans). The bank was granted an additional 2.8% credit quota in December, bringing their current total credit quota to 15.5%, although the bank has prudently grown credit by only 12% as of end-November, choosing not to fully utilise their credit quota.

The November update for VietNam Holding Ltd (LON: VNH) noted that despite inflation and the end of 2% VAT support, retail was the most resilient sector with retailer sales hitting 17.5% year-on-year. They believe domestic consumption growth will normalize around 10% into 2023 with renewed inbound tourism (Christmas and Tet) helping.

VNH also noted that PNJ (the country’s leading jewellery company) performed well in November.

South Asia

India

The Ashoka India Equity Investment Trust PLC (LON: AIE) noted on a year-to-November basis in the Indian market, Utilities and Energy had outperformed, whereas IT Services and Healthcare had underperformed. State-owned enterprises (SOEs) had outperformed their private sector peers, and large caps had outperformed small caps.

For the month of November, Bikaji Foods (snack foods), Kaynes Technology (manufactures electronic components), and Persistent Systems (digital engineering and enterprise modernization) were good performing Indian stocks, whereas Campus Activewear (sports and athleisure footwear), Japanese-Indian automaker Maruti Suzuki, and Titan (manufactures fashion accessories and is part of the Tata Group) were not. On a year-to-November basis, ICICI Bank, Ambuja Cements, and Cholamandalam Investment (consumer finance) were good performers whereas Truecaller (smartphone applications), Mphasis (IT services, outsourcing and consulting), and PB Fintech (online financial services platform) were not.

Meanwhile, the India Capital Growth Fund (LON: IGC) noted for November, India saw a resurgence of Foreign Institutional Investor participation with US$4.7bn of net inflows and the BSE Midcap Index closed at a near all-time high. Large caps outperformed mid-caps with almost all sectors (except auto, consumer durables and power) showing positive performance.

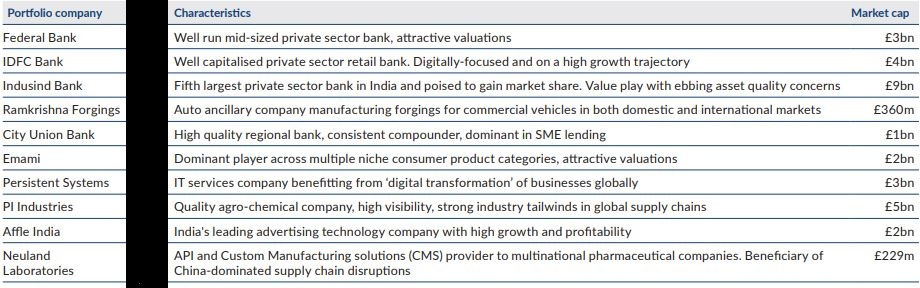

The November IGC update profiled agrochemical stock PI Industries which operates in two business segments – domestic facing agri-inputs business (25% of revenues) and the custom synthesis & manufacturing (CSM) business (remaining 75%):

The former follows an “in-licensing” model with global innovators, registering (a 3-4 year process), manufacturing and marketing “innovator” company products through its distribution network of circa.10,000+ distributors and 70,000 retail points, all under exclusivity. In the latter, PI partners with innovators in their core research and development of new molecules, and when these commercialise, PI becomes a core supplier. PI has a formidable reputation for management quality, technical skills, quality of its facilities and a focus on sustainability. The outlook for PI remains encouraging with a healthy pipeline of new products in both businesses whilst also expanding into adjacent opportunities such as pharmaceuticals and engineering chemicals. It is also winning additional market share as global agrochemical companies shift capacity to India from China and Europe.

The update also contained the following handy table:

Curiously, the JPMorgan Indian Investment Trust plc (LON: JII) November commentary had noted that foreigners remained net buyers of Indian stocks while domestic investors reversed their buying trend from October, recording negative flows. I believe this to be something investors should look further into as it appears this trend has continued.

Financials like HDFC Bank and HDFC Life Insurance had another good month as the banking sector reported strong earnings growth, led by operating profit growth and declining provisions.

Consumer discretionary had a mixed performance as Japanese-Indian automaker Maruti Suzuki and Indian MNC motorcycle and commercial vehicle stock Eicher Motors had volumes that were were muted across segments.

On the other hand, Lemon Tree Hotels performed well as occupancy rates are expected to improve thanks to strong demand drivers and the resumption of foreign inbound travel.

The JII commentary ended by noting:

In our view, the Indian equity story remains in its infancy. While we acknowledge that there will undeniably be volatility along the journey, we also expect this to remain a market where you can find businesses with attractive economics that are sustainable. Coupled with strong governance, this means that the only thing investors need to evaluate is price. In our view, volatility is the friend of the patient investor, and we believe that at points of maximum volatility, investors stand to find the most attractive investment opportunities. The Indian market will no doubt exhibit a level of volatility over the coming years, but we would see this as an opportunity rather than a risk.

SST’s November update hadnoted thatmulti-technology automotive components supplier Mahindra CIE declined after reporting weaker margins due to high energy prices and raw materials cost inflation.

Finally, UEM’s November update noted that state owned oil and gas company Gujarat State Petronet had a good performance on the back of the regulator PNGRB releasing amendments to tariffs (to be implemented in April 2023) that will be beneficial to pipeline operators. This allayed concerns of a material cut in tariffs.

Central Asia

Kazakhstan

BRFI’s November update noted that super-app (as in payments, marketplace, and fintech) stock KASPI was a good performer while commercial savings bank Halyk Bank (with branches in Kyrgyzstan, Georgia, Russia, Tajikistan and Uzbekistan) had an attractive dividend yield.

Middle East

BRFI noted thatSaudi petrochemicals player Yanbu National was impacted by concerns on chemicals pricing from imminent recession.

For November, Barings Emerging EMEA Opportunities PLC (LON: BEMO) noted that Saudi National Bank trended lower due to a controversial October decision to undertake a stake of 9.9% in the Swiss lender Credit Suisse. Saudi bank Al Rajhi posted decent results and strong balance sheet growth, but could not escape regional weakness.

However, Turkish conglomerate KOC had better-than-expected Q3 2022 earnings with the energy division being the main performance driver.

Africa

For November, BEMO noted that global investment group Prosus (majority-owned by South African multinational Naspers), which holds a significant stake in Tencent, rallied substantially in the hope that China would moderate its COVID policies. South African miner Anglo American also outperformed.

Eastern Europe & Emerging Europe

BRFI’s November update noted that Hungarian low-cost air carrier Wizz Air had a good performance after posting strong financial results and guidance driven by improving passenger traffic. Romanian bank BRD also performed well on back of results while Hungarian bank OTP was noted given the decisive monetary measures taken by the central bank there – ahead of the rest of Eastern Europe.

UEM’s November update also briefly mentioned TTS, a Romanian listed river transportation and port operator operating primarily on the Danube River and in the port of Constanta.

BEMO’s November update noted their belief that Greece based Alpha Bank will be able to catch up with its recent underperformance. They also believe management will successfully deploy the capital raised last year and this will fuel underlying credit growth in 2023.

Moody’s has confirmed Greece’s credit ratings. For 2023, the reestablishment of a Sovereign Investment Grade Rating by major rating agencies will help the country lower it’s Cost of Capital.

Latin America

For November, Blackrock Latin American Investment Trust PLC (LON: BRLA) noted that Latin American equity fundamentals improved in 2022 versus 2021 as investors learn to live with the region’s political risk. BRLAalso argued that Latin America seems well-positioned for the following reasons:

- Geographic and economic insulation from the recent global challenges

- Broad exposure to commodities

- Cheap currencies

- Attractive valuations

- Proactive monetary policy (As compared to developed markets, Latin America is considered to be ahead of the curve from a monetary policy standpoint.)

Brazil

BRLA’s November update noted that Brazilian healthcare company Hapvida reported one more weak quarter. The operating environment for the Brazilian health insurance sector remains challenging as medical loss ratios remain high (due to high frequency) and price increases are only starting to slowly come through. Brazilian car rental company Movida also faced a tough competitive environment and a normalization of used-car margins.

On the other hand, they noted that Brazilian exchange B3 was trading on a very attractive valuation and will benefit from any 2023 decline in interest rates. Brazilian bank Bradesco had sold off aggressively on an increase in non-performing loans, but has a strong capital position.

Finally, UEM’s November update noted Brazilian stocks were noticeable decliners during the month (impacted by uncertainty from the new government’s economic policies). Truck, machinery, and equipment rental stock Vamos Locacao was down and logistics stock Santos Brasil was also down despite solid Q3 2022 results.

Mexico & Central America

JEMI’s November update mentioned Mexico had been a positive hunting ground for stocks in 2022, albeit the country’s defensive nature meant it didn’t keep pace in November. They also noted that in November, Mexican financial services group Banorte (Banco Mercantil del Norte) had announced a dividend (and buyback) for a positive signal in terms of how management thinks about capital allocation.

BRLA’s November update notedthat Mexican beverage and retail company FEMSA beat Q3 earnings estimates due to strong operating leverage at its core business (the Oxxo convenience store chain). Panama based Copa airline also saw increased bookings for both leisure and business travellers.

Various Emerging or Frontier Markets

- For November, Mobius Investment Trust PLC (LON: MMIT) noted that Taiwanese IC design house eMemory Technology, Hong Kong-based non-hospital medical service provider EC Healthcare, and Korean manufacturer of critical testing components (for IC production, test and analysis) LEENO Industrial were good performers. Brazilian ERP software firm TOTVS, Indian diagnostic chain Metropolis Healthcare, and Kenyan mobile network operator Safaricom were poor performers.

- For November, the Templeton Emerging Markets Investment Trust PLC (LON: TEM) update briefly mentioned Middle Eastern fast food chain operator Americana Restaurants, India-based online financial services platform PB Fintech, and Dubai-based cooling solution provider Emirates Central Cooling Systems.

That’s it for this week. Hopefully, this post has provided some interesting stock pick or investing ideas to further investigate on your own. Any feedback or comments would be appreciated.

Disclaimer: EmergingMarketSkeptic.Substack.com and EmergingMarketSkeptic.com provides useful information that should not constitute investment advice or a recommendation to invest. Seek a duly licensed professional for investment advice. Your use of any content is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the content. Seek a duly licensed professional for any investment advice. I may have positions in the investments covered. This is not a recommendation to buy or sell any investment mentioned.

EM Fund Stock Picks & Country Commentaries (January 10, 2023) was also published on our Substack.

Emerging Markets Investing Tips + Advice

Emerging Market Skeptic (Website)

Website List Updates + Site Map

Stocktwits @EmergingMarketSkptc

Similar Posts:

- EM Fund Stock Picks & Country Commentaries (June 13, 2023)

- EM Fund Stock Picks & Country Commentaries (December 15, 2024)

- EM Fund Stock Picks & Country Commentaries (May 19, 2024)

- EM Fund Stock Picks & Country Commentaries (November 24 2024)

- EM Fund Stock Picks & Country Commentaries (April 19 2026)

- EM Fund Stock Picks & Country Commentaries (March 16 2025)

- EM Fund Stock Picks & Country Commentaries (December 14, 2025)

- EM Fund Stock Picks & Country Commentaries (October 13, 2024)

- EM Fund Stock Picks & Country Commentaries (June 30, 2024)

- EM Fund Stock Picks & Country Commentaries (July 25, 2023)

- EM Fund Stock Picks & Country Commentaries (February 14, 2023)

- EM Fund Stock Picks & Country Commentaries (December 20, 2023)

- EM Fund Stock Picks & Country Commentaries (January 12, 2025)

- EM Fund Stock Picks & Country Commentaries (May 2, 2023)

- EM Fund Stock Picks & Country Commentaries (January 31, 2023)